The Resilient Investor (2015)

CHAPTER 8

Your Resilient Investing Plan

Designing, Implementing, and Evaluating Your Resilient Investing Plan

WE HAVE COME A LONG WAY TOGETHER, AND YOU’VE BUILT UP A clear understanding of the resilient investing landscape—the new framework of the RIM along with your own worldview and priorities. You are indeed ready to face the uncertainty of tomorrow by having a future-proof portfolio in hand. Now it’s time for the rubber to meet the road.

There are many kinds of travelers. Whether you do comprehensive research and decision making on your own, or tend to collaborate with professionals, or follow an inner compass that points you toward your next destination, we want to help you find a path that will enhance your life while making the world a better place. However you make your decisions, you will want to do all you can to ensure that your choices fully reflect your sense of purpose and long-term goals.

In the pages that follow, we outline a step-by-step process that will help you map your route forward. Of course this is just the skeleton of how it would look in practice—the flesh and blood come from your own reflections and conversations. Whether you follow the structure we lay out here or take a different approach to the process of personal change, you will want to carry these questions with you—to a personal retreat, in conversation with loved ones, on long quiet hikes, or as part of your consultations with trusted advisors. As you do, you are likely to find that the resilient perspective has become integrated into the ways you process new experiences and contemplate the future.

The Power of the Planning Retreat

Making time for careful planning and diligent assessment is not easy; it requires prior thought, commitment, follow-through, and sometimes considerable negotiation with bosses and spouses. But we highly recommend that you plan to take some time away to, uh, plan—we call this the “plan to plan” rule. Cue the planning retreat. It may be a single day or, even better, a weekend that includes periods of diligent thinking, physical activity, and time for quiet reflection.

A periodic retreat is a great tool to facilitate personal growth and make progress on your resilient investing plan; Christopher, one of the authors, aims for at least one a year. Our experience has shown that taking time away from the daily frenzy of life to pause and reflect on progress and challenges brings renewed vigor and enhanced vision to a life well lived. If you want to keep your dance steps fresh, it is an invaluable investment.

STEP 1

Visioning: Where Do You Want to Go?

In chapter 5 you created an initial picture of how you are investing across the Resilient Investing Map, noting your specific investments zone by zone. You have also dug a little deeper and identified which assets are most important, and available, to you. Now the question is: Where do you want to go? Recall this definition from the beginning of this book: investing is something that we all do by directing our time, attention, energy, or money in ways that move us toward our future dreams, using a diverse range of strategies.

It’s time to envision those future dreams and rise up to your full Dancing Diva potential. You have probably been intrigued by a few of the things we mentioned in the previous chapters that you haven’t yet been involved in; and perhaps you have remembered things that you’ve done at some point in the past but are not doing right now.

Looking at where you fall on the spectrum of worldviews about our future has probably generated a bunch more ways to make tweaks and changes. If you see yourself as a Dreamer but you are living like a Dawdler, naturally that suggests a shift in focus. Or maybe you’ve been dealing with it more than you would like; where do you want to take more control of setting your direction? And whatever D you may be, what does the future you see suggest about the mix of strategies you’d like to be involved in as you go forward? For example, if you give the breakdown scenario a high probability, wouldn’t it make sense to have a solid chunk of your investments close to home? Visit the book’s website to complete an online self-assessment that will get you started.

Mostly, it is important to take some time to reflect on the bigger picture of your life. Consider where you would like to see yourself in five years and 10 years. How would you like your life to unfold or change or improve? Think big here! These are the types of questions best pondered over a few weeks. Being outdoors helps, too; a long hike or a weekend at the beach are perfect opportunities to sink into this broader and deeper inquiry. How can you take the self-assessment you did in chapter 5, including your first glimmers of what it will take to become more of a Dancer, and infuse it with this forward-looking visioning?

STEP 2

Explore Your Options

It’s time to turn your attention to specifics: what actions can you take to move from where you are to where you’d like to be? At this stage it’s best to cast your gaze wide and consider a full range of possibilities. After you gather a large number of good investment ideas, you’ll zero in on the most valuable and doable next steps.

So, now that the RIM is modifying how you look at your time and money, what new possibilities or changes have popped up? Do you see one or several areas on your map where you clearly want to do more, whether particular zones or entire rows or columns? Alternatively, are there areas that you’ve been overemphasizing? Jot down anything that you may want to consider adding to each zone in the months or years to come; be as specific or general as you like. Of course, remember that the book’s website has updated ideas and opportunities for each of the nine zones.

In our experience the challenge usually is not finding new ideas—it is winnowing down a hefty pile and filtering the possibilities based on relevance, timeliness, and priority. Many of us feel even more constrained with our time than with our money, given commitments to work and family. Ask yourself, What can I let go of to make room for this? Even if you are excited about your new directions, overextending yourself—your time or money—is never sustainable. Remember that this process is meant to increase your true wealth, so don’t neglect those closest to you, your physical health, or your professional life—keep an eye on all the zones of your map, not just your areas of new focus.

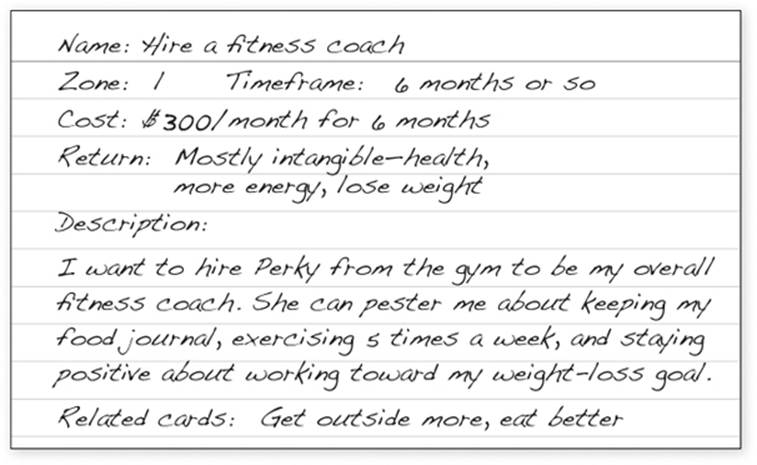

One simple tool that we have found particularly helpful for brainstorming, tracking, and prioritizing a pile of ideas is to use 3 × 5 cards. It is low tech, but it works, especially when you have a lot of new ideas, directions, and life-hacks to consider. Choose the best of the ideas you’ve collected so far; some may require more than one action-item card. Include the most relevant key information on each card: name or title (what are you calling this idea?), what zone it is relevant to, estimated cost, estimated return (if you can determine), brief description of its purpose, estimated time to completion (days, weeks, years), and other cards that relate to a shared goal. Figure 10 shows how Dan the Dealer, a character we will meet in a moment, might fill out a card for one of his zone 1 investments. SEE FIGURE 10

Figure 10 Example of a 3” × 5” Idea Card

Create a 3 × 5 card for each idea; you can work on this in your spare time for a few days or weeks. One nice thing about the cards is that you can fan them out on a table, grouping by zone, column, or row, and experiment with prioritizing and seeing how they work together. After you have played with your cards for a while, it’s time to start making some decisions. Do some further meaningful pruning to bring your list down to a collection of fewer than 10 new goals or opportunities; drop the wacky and promote the wonderful. The top ideas get promoted to the next phase, but keep the other cards; in a year or two, you will want to look back and review them for possible future inclusion.

STEP 3

Prioritize Your Options

Next we select our best ideas and see how we can work them together, including laying out an achievable sequence of steps. The preliminary work can be done in smaller snippets of time, but from here on out you will want to make time for in-depth reflection. Once the designated moment arrives, find a spot outside or by a window with a lovely view, and, if you like, grab a cup of your preferred form of caffeination.

Is there an idea that is jumping up and down with its hand up, just looking for you to call on it? If so, bingo, that’s probably what you should consider first. Looking ahead a year or two, does anything pop out as a natural next step? Perhaps your life is already so well tuned that you need only small adjustments to a couple of zones to help everything sing; see how you can give those areas a nudge. Can you put some things in place right away that will create opportunities for new investments in the following year? Maybe you need to take care of some mundane issues (new roof for the house) before moving on to ideas that truly inspire you. Thinking ahead, are there ideas that would work in three to five years? Seeds that you plant now can germinate and sprout as you find ways to allocate more time, attention, or money to them. Some of your ideas may seem a bit far afield, but with a little skill and luck you could coax them to take root and reap an abundant harvest.

Now that you have oriented yourself, let’s take the process a little further. Consider the following criteria as you continue to organize and prioritize. You do not need to address every one of these considerations; hold them lightly and follow the threads that feel most relevant to your situation.

Time

Which aspects of your schedule can shift to make room for new initiatives? Some actions are as quick as a phone call; others take weeks or years to come to fruition. Balance the time you have available and the level of sustained attention you can give with the demands of the new opportunities you are considering.

Money

What will each new action or investment idea cost? Can you sketch out a budget (rough or precise)? How is your overall budget, and what level of financial burden can you accept? Can you save first before proceeding, or does it make sense to borrow money to make it happen? Could you consider sharing the cost and the resource with others? How about bartering for what you want? Can you reallocate resources from other zones; for example, can you sell some mutual funds to pay for home upgrades?

Return on Investment

Evaluating returns can be a complex project, even for investment advisors! Can you estimate your future income or savings from the new investment ideas you’re considering? Even a rough sketch of returns is helpful (see “Evaluating Nonfinancial Returns” in chapter 5 and Resource 2: The Investor’s Eye at the back of the book).

Personal Skills and Level of Support

Can you implement your choices? If not, can you learn or partner with someone who is skilled? What resources are available that can improve the chances of success? Do you have family members or friends who might be willing to share the work and learn alongside you, such as a buddy with construction skills that complement your own? If you have access to low-interest loans from family or friends, this will obviously make additional investment strategies available to you. What about online community support? Check for individuals, organizations, and businesses that may be a good fit for collaboration.

Professional Assistance

Hiring professionals is another important area for consideration. Even if you are frugal by nature or necessity, it can often be cost-effective to hire expertise rather than try to learn everything yourself. Competent coaching and support can often mean the difference between success and failure.

Now that you have looked a little deeper, done some nipping and tucking of ideas, and settled on your priorities, you are ready to start bringing your new ideas to life—let’s dance!

STEP 4

Sequencing: Choreograph Your Dance

Your choreography will lay out the first few action steps, say, over the first six months, then another objective or two in the next year or so, and then any additional projects to be activated over the next three to five years. You can always improvise around whatever structure you lay out, but having a basic framework will help you keep the big picture in mind. Stack those 3 × 5 cards in order or just make a list. Rough out your dollar estimates next to the ideas or note if you need to do a little more research; likewise consider the time commitments for each and whether the demands on your time will be regular or episodic. Double-check that the way you have laid things out makes sense; relying on this master action-item list will keep you on track.

Now is the time to begin drafting your new RIM; transfer your current and new ideas onto a fresh map and see how it all fits together. To see how that looks in practice, let’s take a look at a couple of examples. We will meet Dan, who filled out the 3 × 5 card in figure 10, and also check in on Dahlia and Adele, whose first-round RIMs we saw in chapter 5. The following RIM examples include just their new activity; you may want to create a more complete map that includes all of your existing and new investments.

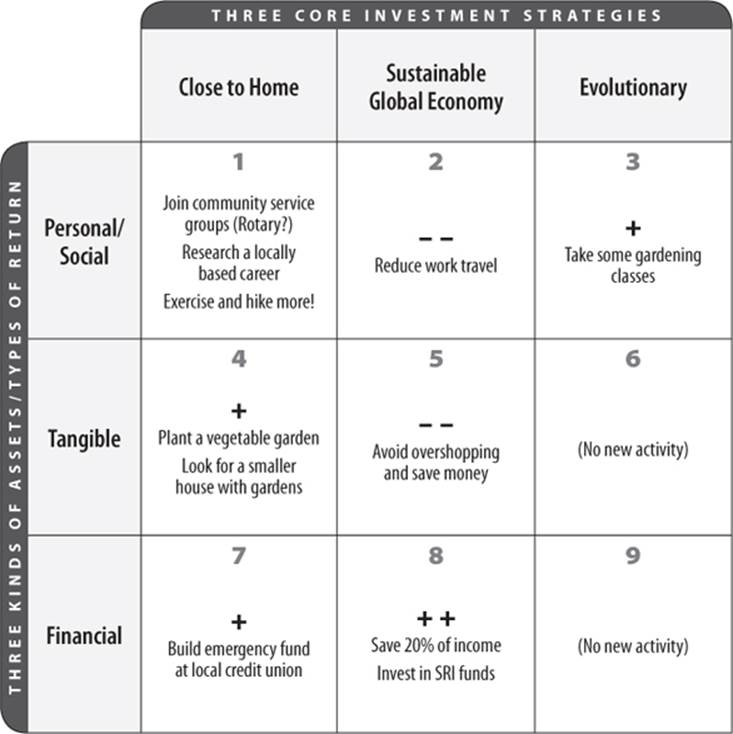

Dan the Dealer

Through exposure to the RIM, Dan the Dealer, who has a 9-to-5 sales job, realizes that he has been concerned about the state of the world (and his life) and decides to become more self-sufficient and connected to his home community. SEE FIGURE 11 Here is his sequence of implementation for the next couple of years:

![]() Immediately: start saving 20 percent of his net income, invested in a blend of SRI mutual funds that hold both bonds and stocks (zone 8)

Immediately: start saving 20 percent of his net income, invested in a blend of SRI mutual funds that hold both bonds and stocks (zone 8)

![]() Six months: scale back sales travel (zone 2); join a couple of community groups (Rotary? Transition town?) (zone 1); plant a garden in the backyard (zone 4)

Six months: scale back sales travel (zone 2); join a couple of community groups (Rotary? Transition town?) (zone 1); plant a garden in the backyard (zone 4)

![]() One year: investigate a more local occupation and career (zones 1 and 2); lose 25 pounds by exercising and hiking more with his son (zone 1)

One year: investigate a more local occupation and career (zones 1 and 2); lose 25 pounds by exercising and hiking more with his son (zone 1)

![]() Three years: investigate buying a smaller house with enough land to grow food (zone 4)

Three years: investigate buying a smaller house with enough land to grow food (zone 4)

Figure 11 Dan the Dealer’s Mixed RIM

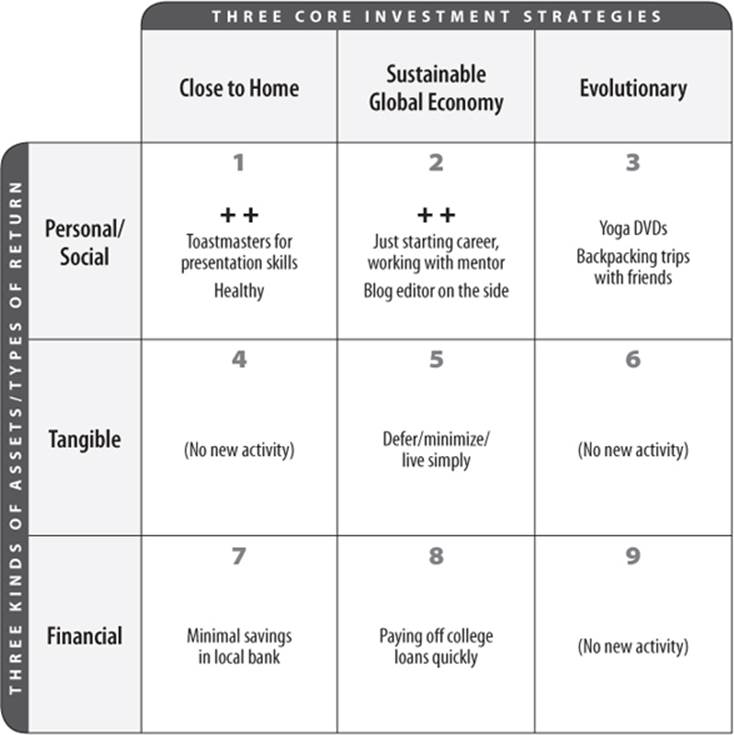

Dahlia the Driver

Dahlia the Driver’s top priority is pushing herself at work to learn quickly and improve her career prospects. SEE FIGURE 12 She’s also attending a local Toastmasters group, improving her presentation skills, and volunteering (for now) as a blog editor to help build and diversify her skills. Paying off her college loans is her second most important goal over the next couple of years, and she is limiting her zone 5 purchases to help improve her financial situation.

Figure 12 Dahlia the Driver’s Dancing RIM

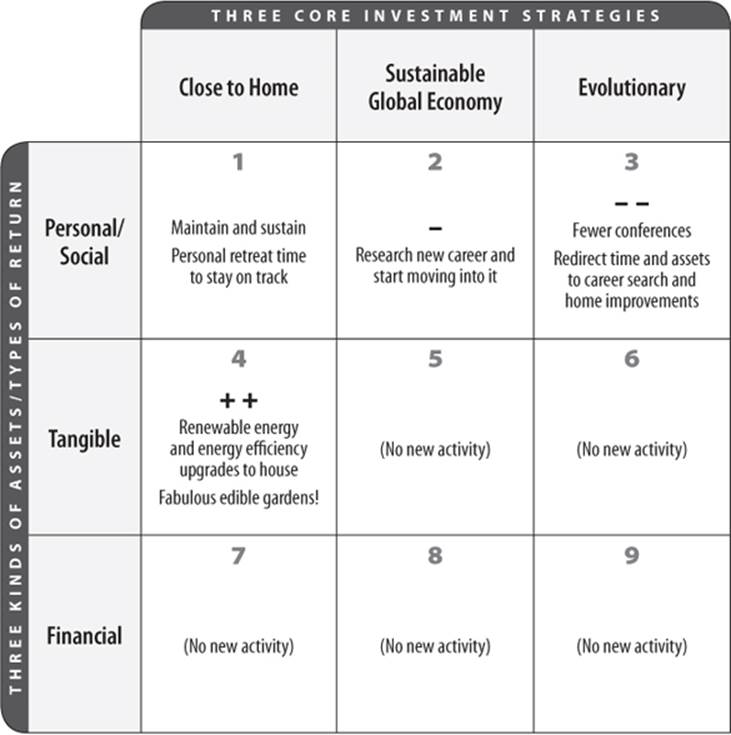

Adele Adaptability

Adele Adaptability is a Dreamer who now realizes that she wants to become more of a Dancing Dreamer. SEE FIGURE 13 During her RIM inventory, she noted that her house could be more energy efficient (zone 4) and that although her backyard has lots of sun, it has mostly been taken over by roses and dandelions. The big burr under her saddle is her job: she is making good money, but she is not very inspired by her career (zone 2).

As soon as she started filling in the RIM, her home and livelihood really popped out at her. Her first investment will be an energy audit for her house—and she is committed to spending a few thousand dollars to improve whatever problems the audit uncovers. She is going to talk with a career consultant to begin the process of realigning her career with her Dreamer aspirations and has scheduled a resilient investor planning retreat to keep herself on track.

Figure 13 Adele the Dreamer’s Dancing RIM

Her sequence might look something like this:

![]() Six months: energy audit and appointment with career counselor

Six months: energy audit and appointment with career counselor

![]() One year: do basic energy efficiency upgrades to the house and work on some of the things the career counselor suggested

One year: do basic energy efficiency upgrades to the house and work on some of the things the career counselor suggested

![]() One to two years: attend one fewer personal growth workshops (for a savings of $1,000) to redirect capital and time into developing career options

One to two years: attend one fewer personal growth workshops (for a savings of $1,000) to redirect capital and time into developing career options

![]() Three years: move into a new job and plant the backyard with fruit trees and planter boxes for tomatoes and lettuce

Three years: move into a new job and plant the backyard with fruit trees and planter boxes for tomatoes and lettuce

Are you beginning to see some possible paths of your own? What can you do in the next six months, year, and three years? What can you stop doing—to free up time, attention, and possibly cash—to fuel your next steps? As you move toward completion of the design phase, make dates with yourself to periodically return your attention and focus to fine-tuning your plan.

STEP 5

Stepping Out: It’s Time to Dance!

Now that you have crafted a solid and resilient plan of action, it’s time to step onto that shiny dance floor! We have four core suggestions that are relevant for almost anyone implementing ambitious new plans.

![]() For any new endeavor, start small to help limit risk and improve the chances of success. When you are learning, don’t take too big of a bite so that you make the inevitable errors with fewer dollars or less time at risk. We like using small-scale trials to test new ideas and activities.

For any new endeavor, start small to help limit risk and improve the chances of success. When you are learning, don’t take too big of a bite so that you make the inevitable errors with fewer dollars or less time at risk. We like using small-scale trials to test new ideas and activities.

![]() We strongly urge people to schedule tasks, especially anything that is new or outside your normal routine. When you are at the end of the planning process, make a point to add next steps to your calendar, and don’t be afraid to set deadlines.

We strongly urge people to schedule tasks, especially anything that is new or outside your normal routine. When you are at the end of the planning process, make a point to add next steps to your calendar, and don’t be afraid to set deadlines.

![]() The relative speed and perseverance of tortoises and hares aside, there is not much argument against slow and steady being the mantra for long-term goal accomplishment. Racing around and forcing more urgency into life is no fun, and it’s not sustainable.

The relative speed and perseverance of tortoises and hares aside, there is not much argument against slow and steady being the mantra for long-term goal accomplishment. Racing around and forcing more urgency into life is no fun, and it’s not sustainable.

![]() And remember that the goal here isn’t just productivity and task accomplishment; cycle through again and dare to dream big! The actual phrase we use is dream big, start small, which reflects a lovely practical-visionary combination. If you are considering a bigger transformation, such as changing your career or moving to a new town or property, give yourself plenty of time to prepare.

And remember that the goal here isn’t just productivity and task accomplishment; cycle through again and dare to dream big! The actual phrase we use is dream big, start small, which reflects a lovely practical-visionary combination. If you are considering a bigger transformation, such as changing your career or moving to a new town or property, give yourself plenty of time to prepare.

If you are challenging yourself as we hope you are, there will be some steps you’ve slotted into your choreography that are new to you. One of the great benefits of the Internet age is the ubiquity of information; it is easy to learn how to do almost anything! Make use of this free guidance, but be sure to confirm how reliable and experienced the sources are.1

STEP 6

Dancing till Dawn: Evaluate, Modify, Repeat

The final step of the design process is to keep on dancing! Central to the resilient part of being a resilient investor is a process of evaluation and tweaking of your plan as the years go by. Periodically, you will want to look back at how your plan performed and take a fresh tour through all these steps as you adapt your plan for its next stage.

How has the past year been? Overall, what has gone well? Were there challenges? More specifically, how did the new investments or ideas that you implemented in the past year turn out? Successes? Failures? Are there things that are on track as is or that could use a slight nudge? What should be discontinued? Review your plan or plans from previous years: what had you set out for yourself to be working on in the coming year or two? Take some time to sit comfortably, contemplate and reflect, and take notes.

You will want to devote time and focus to evaluate both successful investments and those that haven’t turned out as planned. Perhaps some new ideas or investment opportunities have become available that you can now include. Has your view of the world—and the future—shifted? Maybe you now identify with a different D-type or your availability of time and money has changed. Modify your plan or create something completely new: it’s your life; make it what you want!

Every journey begins with a single step, and now you are well along the road you have chosen. You’ve learned how to see your life through this expanded view of investing and embraced the goal of becoming increasingly resilient as the years go by. Make a celebratory list of everything that has moved forward since your previous planning session—and put it on your wall to remind you that each day is a chance to dance your way toward your dreams.

All materials on the site are licensed Creative Commons Attribution-Sharealike 3.0 Unported CC BY-SA 3.0 & GNU Free Documentation License (GFDL)

If you are the copyright holder of any material contained on our site and intend to remove it, please contact our site administrator for approval.

© 2016-2026 All site design rights belong to S.Y.A.