Valuing and Selling Your Business: A Quick Guide to Cashing In (2014)

Chapter 2. Valuation Fundamentals

Valuation in Plain English

“I don’t want to pay that much for a valuation,” the caller said. “Can’t you just put my numbers into the computer and spit out my value? I just want something quick and dirty.” This is an all-too-common conversation that I have with potential clients. The truth is, there’s no such thing as a quick valuation, and there’s no (reputable) computer program that can provide an accurate valuation based on a bunch of numbers you input.

In this chapter, I will explain the entire valuation process by using everyday language. So if you are a valuation professional, please forgive me for not using the specific nomenclature that you are used to.

Let’s look at a real-life example that shows why a good valuation depends on much more than looking at only financial records. There is a national parts distributor that buys products directly from manufacturers and then processes and repackages the products and delivers them to the retailer. The retailer then sells the products to the consumer. Historically, the distributor’s revenues have been over $100 million and the annual profits have been consistently over $4 million.

How much is this business worth? Should it be based on a percentage of revenues? How about a multiple of earnings?

The actual value of this business is less than $1 million. How can this be? Based on historical earnings, you would earn the purchase price in three months. What a bargain! Interested?

The rest of the story is that the distributor is very dependent on one customer. That customer accounts for over $90 million (or 90%) of the $100 million in annual sales. They recently lost the customer and may liquidate the business rather than try to rebuild it. After selling the company’s assets and paying off all the company’s obligations, the owner believes that he will be able to put just less than $1 million into his pocket. This process will take a couple of years.

Would you get the right answers if you simply put numbers into a spreadsheet and based the value on historical earnings? Absolutely not! Why? It’s because of the following point:

![]() Important Valuation is a prophecy of the future based on the information that the valuator has as of the valuation date.

Important Valuation is a prophecy of the future based on the information that the valuator has as of the valuation date.

If someone has prepared a valuation for you by using a canned valuation software program without interviewing you and without understanding your business and industry, please take the valuation report and throw it in the trash. It’s not worth your time.

The valuation process is a mystery for most business owners. Web sites, articles, and books like this one can shed light on the mechanics of placing a value on a business and will provide you with some education on how to value a business. However, the terms used in many of these resources makes the valuation process seem more complex than it actually is.

Some business owners will hear stories from their friends or read articles about how much money others have received from selling their business. “It was simple,” says the friend. “They gave me five times earnings.” This makes the valuation process seem easy.

The reality is that the valuation process is much more involved than multiplying an earnings number by a multiplier, but it is not so complex that you cannot understand it.

Hopefully after reading this chapter, you will have a basic understanding of the valuation process and be able to explain to your spouse in plain English this process. You will also know the difference between enterprise value, equity value, and the net proceeds that you receive after you sell your business. The discussion is still more of an overview, but a necessary one. In the next chapter, we will dive in deeper and provide more of a “how the sausage is made” explanation of the valuation process.

What Is a Business Valuation?

A business valuation is a process and a set of procedures used to estimate the value of an owner’s interest in a business. The key words in this definition are process, procedures, and estimate.

A long-standing resource that describes business valuation and the important factors in the valuation process is IRS Revenue Ruling 59-60 (usually known as 59-60). When it was introduced in 1959, 59-60 was the most important resource in determining how to value a business. It has stood the test of time and continues to provide a guide to business valuators on how to prepare a valuation for the IRS and for other purposes. The following is a key excerpt from 59-60:

Valuation of securities is, in essence, a prophecy as to the future and must be based on facts available at the required date of appraisal.

Let’s break down this definition further. Valuation is an estimate of value. Of the 2,000+ valuation engagements that I have been involved in, there have been only a handful of times that an actual sale of the appraised business occurred within a few months of the valuation date. Almost 100% of the time, I had no verification of how close my estimate of value would be to reality. In part, that’s because many are done for estate planning purposes, divorces, and other efforts that do not involve the sale of the business.

I’ll be the first to say that valuations are subjective. The IRS concurs, to a degree. The opening paragraph of 59-60 states the following:

In valuing the stock of closely held corporations, or the stock of corporations where market quotations are not available, all other available financial data, as well as all relevant factors affecting the fair market value must be considered for estate tax and gift tax purposes. No general formula may be given that is applicable to the many different valuation situations arising in the valuation of such stock. However, the general approach, methods, and factors which must be considered in valuing such securities are outlined.

How do you know if the conclusion is correct? Unfortunately, you don’t. And this is where the next part of the definition is important. There are recognized processes and procedures that are standard in the business valuation industry.

Therefore, a business valuation is much more than simply putting numbers into a spreadsheet and spitting out a number. If a valuation is an estimate based on a prophecy of the future, how is this done? With a crystal ball? Dartboard? Truthfully, these may provide you with more insight than an analysis prepared by untrained professionals using computerized software.

Before we dive into the recognized processes and procedures of a business valuation, let’s discuss the business valuation profession and when a business valuation is needed.

The Valuation Profession

When you need a business valuation, where should you go? To your CPA who prepares a few valuations a year, aided by his latest and greatest software program? To an Internet provider that promises you cheap and fast valuations? Or what about those professionals who travel around the country leading slick seminars that will get you all enthused about selling your business? Of course, those “professionals” also want you to sign up for only a $55,000 business valuation to start the process.

So how do you decide who will prepare the valuation of your business?

Business valuation has become its own profession. There are four major professional organizations that provide training and accreditation to the business valuation profession. For each one, the accreditation process includes testing on valuation theory and standards, submission of work product, and an experience requirement. Some designations are harder to obtain than others (e.g., ASA); however, if someone has a designation from one of the following four organizations, you can know that the valuator understands the recognized processes and procedures used in a business valuation:

· ASA (Accredited Senior Appraiser) by the American Society of Appraisers

· ABV (Accredited in Business Valuation) by the American Institute of Certified Public Accountants.

· CVA (Certified Valuation Analyst) by the National Association of Certified Valuators and Analysts

· CBA (Certified Business Appraiser) by the Institute of Business Appraisers

A business valuation incorporates many different disciplines and requires the valuator to have a variety of skill sets. Valuators or their teams need to be familiar with the following in order to produce a credible business valuation:

· Know how to read financial statements and understand accounting theory.

· Understand how income taxes impact value.

· Know the relevant tax codes and court cases on valuation issues.

· Be able to perform robust financial analyses.

· Understand how the economy will impact a business’s cash flow.

· Have a firm grasp of valuation theory and be able to apply the appropriate valuation methods.

· Be able to research complex issues.

· Know how publicly traded stocks are valued.

· Be able to communicate the results of a valuation to a business owner, a judge, or the IRS.

In addition to these skills, the valuator needs to apply “common sense” and be unbiased. At the end of the day, the valuator should step back and ask the question: “Would I buy the business at the price I valued it?” At times, it is clear to me that a valuator’s conclusion is not remotely close to the actual value. This is typically due to a valuator’s lack of knowledge or experience, or a decision to provide a biased opinion of value. At times, business valuators can become advocates and manipulate the results in order to please their client.

It will be difficult for you to determine the skill and the common sense of the business valuator. So how do you objectively hire the right person for you? Of course, I am biased, but I suggest that you look for the following when hiring a business valuator:

· It should be a full-time profession and not something they do occasionally to supplement their income.

· They should have at least two designations from the organizations listed previously.

· Experience is a critical factor, similar to choosing a surgeon. You don’t want your company to be one of the valuator’s first projects. You should select someone who has been involved with hundreds of valuation projects.

· They should be able to explain complex business issues to you in plain English. They should also be willing to sit down with you and your family members and explain how the valuation was prepared and why they chose a certain conclusion. You want someone who enjoys teaching clients about the valuation process.

· Valuators should be willing to defend their work. I have testified at trials and depositions dozens of times, and it is not easy defending your work in stressful situations. Not all valuations end up in conflicts; however, it is good to know that your valuator will not fold under pressure if the IRS or anyone else questions the valuation.

· Ask for recommendations from professionals and other business owners. Bankers, CPAs, lawyers, and investment advisors are good professionals to ask.

Once you select a valuator and subsequently receive your report, ask yourself these questions when reviewing the valuation:

· Did the valuator really understand the business?

· Did the valuator consider the future industry trends and how the business will perform in different economic cycles?

· Did the valuator use widely recognized valuation methods?

· Does it appear that the valuation is a prophecy of the future?

A valuation report prepared by a member of one of the organizations listed previously is required to follow certain reporting standards. In order for you to understand what should be included in your valuation report and the definition of some the terms typical used in a valuation, I have included a summary of the valuation reporting requirements from the AICPA Statement on Standards for Valuation Services No. 1 and a glossary of valuation terms (see Appendix C).

![]() Tip This final question needs to be asked after reviewing a business valuation: Would you buy the business at the price that the valuator concluded? If so, the valuation is probably realistic.

Tip This final question needs to be asked after reviewing a business valuation: Would you buy the business at the price that the valuator concluded? If so, the valuation is probably realistic.

When Is a Valuation Needed?

Valuations are needed in a variety of situations. If someone dies and owns stock in a company, the IRS wants to know the value to determine any estate tax owed. If a business owner is going through a divorce, the husband and wife both need to know the value in order to correctly split up the assets.

In my practice, I categorize business valuations into two different camps. The first is the “have to” valuations, and the second is the “should” valuations. The former valuations are driven by a specific event (i.e., death and divorce). The latter are valuations not driven by an event, but based on the business owner’s desire to know the value of the business. Business owners need to know the “real value” in order to develop succession and estate plans, take steps to increase value, and properly position the business for a sale. In another words, they want a valuation in order to treat their business like an investment.

“Have To” Valuations

The majority of my valuation practice, as well as with other valuation professionals, involves preparing “have to” valuations. In these cases, there is an event that drives the client to pick up the phone and call a valuation professional, such as the following:

· Death of a shareholder: When a business owner dies, there are various parties that need to know the value of the decedent’s interest. If the business owner’s estate is large enough, the IRS requires an estate tax return to be prepared and the estate must send it a valuation that meets the 59-60 standards. For smaller estates, the heirs, other shareholders, and probate court will want to know the value.

· Gifts of closely held stock: A popular exit strategy is to gift stock of a closely held business to the next generation. Again, 59-60 must be followed in order for the gift to be accepted by the IRS. If the valuation meets the IRS standards, there is a three-year time period in which the IRS can question the value. After that, the IRS cannot make adjustments. If the valuation does not follow 59-60, there is no statute of limitations and the IRS can come back 5, 10, or 20 years later and impose additional taxes and penalties on the gift.

· Equity compensation valuations: If a business provides an equity incentive plan to their employees (including stock options or stock bonuses), a business valuation needs to be prepared. These incentive awards are considered to be compensation to the employees and the compensation level reported to the IRS is determined by a business valuation.

· Dispute related to valuations: There are two types of disputes that business valuators typically get involved with: divorce and shareholder disputes. If a business interest is a marital asset, it has to be valued just like any other marital asset. It is rare when the business owner and the spouse just divide and each retain the stock in a company. Instead, once a value is determined, the business owner writes a check to the spouse for his portion of the business value and she keeps the company. Shareholder disputes are just as common as divorce valuations. If shareholders want to leave a business or are forced out, they need a valuation to determine the value of their ownership interest.

As you can imagine, these valuations can be quite adversarial. Sometimes, the parties hire one valuation professional who acts like a mediator and the valuation issue is resolved quickly. Other times, the parties hire their own valuation expert and each side “dukes it out” in court. Then a judge with no business background decides what the company should be worth.

· ESOPs: An ESOP is a qualified retirement plan where the employees own the stock. A valuation is required when the ESOP is established and also is required on an annual basis. When the ESOP is established, a valuation is needed to determine the buy-out price paid to the shareholder selling to the ESOP. After that, there are annual ongoing valuations that set the price per share that gets allocated to the employees’ individual accounts. When employees leave the company, their shares are bought out based on the annual valuation.

· Other situations that require a business valuation: This is not all inclusive, but these are other events that will require the business owner to obtain a business valuation: bankruptcy, converting from a C-Corporation to an S-Corporation, a charitable contribution of closely held stock, or an allocation of intangible assets after buying another business.

“Should” Valuations

Some valuations are not driven by a specific event but are important for the business owner to have. There is no court date, IRS deadline, or anything else that drives the business owner to pick up the phone and hire someone to prepare a business valuation.

These valuations are used by business owners to make important decisions about their future. We have discussed why this is important in the opening chapter of this book. The following are some specific reasons why business owners have hired us to prepare valuations that are not based on a specific event:

· Estate planning

· Succession planning

· Selecting the appropriate exit strategy

· Determining life insurance needs

· Looking for ways to increase the value of the business

· Setting a value in a buy-sell agreement

· Setting up incentive plans for management

There is another reason why we are hired for a valuation project that is in-between the “have to” and “should” valuations. This is for merger and acquisition (M&A) purposes. There is no requirement that you obtain a business valuation when someone wants to buy your business. But certainly it would be wise to have a professional assist you when you are thinking about selling your most valuable asset. The same goes for buying a business. You can pay what you want. But if you are going to make a major investment, it would be wise to have a trained set of eyes providing you with advice on how much you should pay.

Now that you have an understanding of the valuation profession and when a valuation is needed, it is time to talk about the valuation engagement.

The Valuation Engagement

I am amazed at how often business owners obtain a business valuation, and it does not deliver what they need. This is due to a misunderstanding at the beginning of the process. The business owner does not understand what is being valued and the standard of value being used. Any valuation engagement should be spelled out in the beginning of the process with an engagement letter. This step ensures that the valuator and the business owner are on the same page (see example in Appendix A). These are the four major areas that should be clarified in the engagement letter:

· What is being valued

· How the value is defined (standard of value)

· The date of the valuation

· The purpose of the valuation

What Is Being Valued?

The first question a valuator should ask a business owner is, “What are we valuing?” A common response from a business owner is this: “What do you mean by what are we valuing? Just tell me what my business is worth, so I can see if I can retire.”

Unfortunately, many business owners are unpleasantly surprised at the level of proceeds they receive from the sale of their business. They expect a certain amount of dollars after the sale but can receive significantly less when the deal is done. How can this be?

This is due to two factors. The first is a lack of understanding of the difference between enterprise value and equity value. The second is that the seller did not factor in the impact of income taxes and transaction costs. This is very important to understand. To make sure this is clear to you, I have added examples at the end of this chapter.

Enterprise Value vs. Equity Value

Enterprise value is simply the value of the business operations. Sometimes it is called the operating value. Enterprise value includes the company’s working capital, fixed assets, goodwill, and other intangible assets. It excludes the value of assets that are not needed to operate the business (nonoperating assets) and almost all liabilities except accounts payable and accrued expenses. For example, any long-term debt with a bank is excluded when determining the enterprise value. Enterprise value is typically the selling price for the business operations.

The equity value is the value of the stock of a company. It is determined by adding to the enterprise value any nonoperating assets and subtracting out the obligations of the company that are not typically assumed by the buyer of the business. Equity values are often calculated in the case of divorces and for estate planning purposes. Here is the formula for determining the equity value:

Equity Value = Enterprise Value + Nonoperating Assets – Liabilities Not Assumed

Nonoperating assets are items that are owned by the business that are not necessary for the day-to-day operations. Examples of nonoperating assets include vacation homes, luxury cars, excess cash, and life insurance cash surrender value.

Typically a buyer of a business will assume a limited amount of liabilities (accounts payables and accrued expenses). After the transaction, the seller pays off the other obligations of the company, including any bank debt.

The valuator and the client need to clarify what value is needed—the equity value or the enterprise value.

Net Proceeds from a Sale of a Business

In Chapter 5, we will discuss the difference between an asset sale and a stock sale. There is a huge difference between the two. Under an asset sale, the proceeds received from the sale are collected through the business entity and the business is liquidated. Then the remaining proceeds after paying off all retained debt and liabilities are distributed to the equity owners. In a stock sale, business owners simply sell their stock and walk away. This option is much simpler and better for the seller, but a stock sale rarely occurs. For now, we will focus on what happens with an asset sale.

Under an asset sale, the proceeds from selling the business’s operating assets are paid to the business entity. The amount received is reduced by transaction costs and paying off all remaining liabilities. Transaction costs include fees paid to business brokers, lawyers, and accountants. Before business owners can spend or invest the proceeds from the sale, they have to factor in the tax consequences of the transaction. The amount of the total taxes owed depends on many factors and can be up to 50% of the selling price. Tax consequences on asset and stock deals will also be explained in more detail in Chapter 5.

Another issue that should be clarified at the start of the valuation process is what percentage of the business entity is being valued. Is it a 100% interest or something less than that? A minority interest is a stake in a company that is less than 50%. It is worth less on a per share basis than a controlling interest. This is due to the severe limitations that minority owners have. We will talk more about this in the next chapter.

How the Value Is Defined

There are a few different standards of values that are used in the valuation profession. Standard of value simply means how value is defined. It is very important that business owners understand which standard of value was used for their valuation conclusion. The valuation conclusion will not be the same for each standard of value. In this book, I will only focus on the “fair market value” and the “investment value” standard of value.

Fair market value is defined as the cash or cash equivalent price at which property would change hands between a willing buyer and a willing seller, neither being under a compulsion to buy or sell, and both having reasonable knowledge of relevant facts.

Investment value is defined as the potential value to a strategic buyer. A strategic buyer is one who can realize synergistic benefits through the combined purchasing power of the new entity and the elimination of duplicate functions or competitive factors. Investment value is typically higher than fair market value. Sometimes it is called synergistic value.

Fair market value assumes that the buyer of a business will step into your shoes and have the same opportunities and cash flow that you have. Investment value assumes that the buyer will be able to make significant changes that will positively impact future cash flow.

Fair market value is used for most of the “have to” valuations. The IRS and the court system want to know the value based on current operations and not what the value is to a larger company that can achieve synergies from the purchase of the business.

Investment value is used in situations where the business owner wants to sell the business for top dollar and is curious what a larger business that can eliminate jobs and has other synergies will pay for the business. In these cases, we attempt to determine what the synergies will be to the buyer and anticipate their future cash flow. Sometimes a buyer is just interested in the seller’s intellectual property (patents, software developed, etc.) and is willing to pay large dollar amounts even though the seller has not been profitable, owing to the buyer’s ability to better utilize these assets and increase their cash flow.

This is why it is important to know what standard of value is used in the valuation. Sometimes I will show the business owner the value under both the fair market value and the investment value standard. This is helpful in choosing what exit strategy makes the most sense. Some business owners want top dollar for their business and are willing to sell to a larger business, even though they know it means many jobs will be eliminated. Other business owners are willing to accept a lower selling price if they are assured that their employees will keep their jobs.

The Purpose of the Valuation

Earlier in this chapter, we discussed the reasons someone may need to have a valuation prepared. It is very important that the purpose of the valuation be clear in the beginning of the process since the standard of value used is based on the purpose of the valuation.

In addition, there are many times when someone will try to use a valuation done for one purpose for another purpose or the valuation prepared for one purpose gets used for another purpose. I hate it when I get calls from divorce attorneys saying that they have a copy of a valuation done for business planning purposes and they want to use it in a divorce case. Is the valuation conclusion the same? It depends on the standard of value used and the date of the valuation.

The Date of the Valuation

The valuation is always as of a specific date. The determination of the valuation date is very simple in the case of an estate (day of death) or gift (date of the gift) but can be much harder to determine in other cases. A divorce is an example of where the date can be confusing. Is it the date of separation? The date of the final court hearing? It is important that the date of the valuation is clearly established between the valuator and the client.

In valuation theory, events that occur after the date of the valuation should not be considered unless they are reasonably foreknown. One day can make a big difference in the valuation conclusion. A company with a devastating fire that was not properly insured is worth significantly less the day after the fire than it was the day before.

Now that you understand what needs to be clarified before starting a valuation engagement, let’s discuss the relevant factors that should be considered during the valuation process.

Important Factors to Consider in a Valuation

Valuing a business is not a simple and quick process. There are many factors that need to be considered before coming to a conclusion on a company’s value.

The following is an excerpt from IRS Revenue Ruling 59-60:

It is advisable to emphasize that in the valuation of the stock of closely held corporations or the stock of corporations where market quotations are either lacking or too scarce to be recognized, all available financial data, as well as all relevant factors affecting the fair market value, should be considered.

What are the relevant factors? The following is not an all-inclusive list of the relevant factors, but these factors are fundamental and require careful analysis in each case:

· An in-depth understanding of the business: Valuation analysts need to know all they can about the business and its operations. This includes knowing the strength of the management team, the products and services sold, the customers, the suppliers, what keeps management awake at night, and what they are excited about. This is very important in determining how risky it is to buy the business and what “rate of return” the buyer requires in order to make an investment in the business.

· Historical financial trends of the business: During the past few years, has the business been growing or declining? Are the profit margins improving or deteriorating? Are the financial results consistent or unpredictable? Will these trends continue into the future?

· Economic outlook where the business operates: The revenue and profit of some companies are tied directly to the overall economy of where they operate (e.g., a construction-related company). The expected future operating results are tied directly to the forecast for the economy. Meanwhile, other companies are not impacted by how the overall economy is doing because they have developed products that sell in good and bad times (e.g., Apple).

· Industry outlook: Understanding the outlook of the specific industry where the business operates is critical in any valuation. For example, in the 1980s typewriting manufacturers may have had very good historical financial trends; however, the outlook for the industry was poor due to the acceptance of the personal computer and word processing software. Within a few years, there were no longer any manufacturers of typewriters.

· Management’s forecast of the future: Valuation is a prophecy of the future. It is critical that the valuation analyst spend a great amount of time discussing with management their expectations for the future and understand any reasons why it may deviate from recent historical trends. The valuator needs to have a skeptical mind when dealing with management forecasts and make a judgment call whether to believe them or not. This is particularly true when management wants a certain outcome. For instance, is it a coincidence that owners talk about all the bad things happening to their business, and how the future will be much worse than the past, when they are going through a divorce?

Only after valuators believe that they have a good understanding of a business and its prospects for the future can they begin determining the value of a business.

The Three Valuation Approaches

In my profession, there are three recognized approaches in determining the value of a business. Under each approach, there are many different accepted methodologies in determining value. The three approaches to value are the income, asset, and market approach. In the next chapter, we will discuss these in more detail.

The Income Approach to Value

This is the most widely used and accepted approach in valuing a business. In the simplest terms, this approach determines the future economic benefit the buyer will obtain from buying the business and then determines the rate of return required to entice an investor to buy the business. This is similar to any other investment that you may consider investing in. Two questions need to be asked: what can I earn on the investment and how risky is that investment?

The Asset Approach to Value

This approach estimates the value of the tangible assets owned by the business (cash, receivables, inventory, and equipment) and the amount of the business’s obligations (payables, payroll, taxes, and bank debt) as of the valuation date. The difference between the value of the assets and the obligations is the value under this approach. When this approach is higher than the other approaches, it means the business is worth more dead than alive and the valuator should factor in the cost to liquidate the assets into cash in determining the final value.

The Market Approach to Value

The most effective way to appraise your house is to find the sale price of other houses in your neighborhood that have recently sold. The market approach to value a business is similar to what real estate appraisers do. The valuator tries to find companies that are similar to the business being valued that have sold in the marketplace or are publicly traded. My firm subscribes to various databases that provide us with information about private company transactions. For some businesses, like a McDonald’s restaurant, it is easy to find transactions and make the comparison to determine value. While for others, like a niche manufacturer, it is more difficult to find a comparable company and use the market approach.

We will discuss which approach makes the most sense in the valuation engagement in the next chapter. Many appraisers make the mistake of averaging the three approaches. This rarely is the best way to form a conclusion of value.

Valuation Definitions

At the end of the chapter, I present some very basic calculations that will enable you to understand the difference between enterprise value, equity value, and net proceeds. But first you need to understand two other concepts that will help you better understand these examples.

· Sustainable cash flow: This is the forecasted cash flow level that buyers expect to be able to put into their pocket on an annual basis. The sustainable cash flow is what is available after all expenses and taxes are paid and funds are retained for making investments into capital items (e.g., equipment). It is the cash produced by the business over and above what is needed to sustain operations. In other words, it is what the business owner can spend or invest.

· EBITDA: This popular financial acronym stands for “earnings before interest, taxes, depreciation, and amortization.” It is how much cash is available before paying taxes and making investments into equipment, trucks, and other capital items. The term EBITDA is widely used in the valuation profession. A popular way to determine the enterprise value is taking the company’s EBITDA level and multiplying it by an EBITDA multiplier, which changes depending on the industry, risk factors, and growth rate.

Valuation in Plain English

Armed with those two definitions, let’s proceed. Remember that one of the most important concepts in valuation theory is that valuation is a prophecy of the future. Prophecy of what? It is the prophecy of the economic benefit available to the business owner. In other words, it is how much they pull out of the business on an annual basis and spend or invest.

When someone buys a business, there are two main questions that need to be answered before determining what price to pay for it:

· How much cash will I put into my pocket from buying this business? (This is the sustainable cash flow.)

· How sure am I that it will go into my pocket? (This is the required rate of return related to the sustainable cash flow.)

The buyer will perform, or hire someone to perform, a detailed analysis to answer these questions.

How Much Cash Will I Put into My Pocket?

The starting point in determining the sustainable cash flow is to normalize the historical financial statements. With this step, I make adjustments for unusual or nonrecurring items that would cause any particular year not to be truly representative of the operating results. For example, a one-time settlement payment from a lawsuit of $500,000 is not a recurring item and part of normal business operations. The next chapter will include more extensive information about the normalized process.

The normalized process provides us with historical financial trends that exclude items that are not part of the normal business operations. Does the historical normalized financial statement provide us with the best indication of the future? It might. It depends on what we learn from our study of the industry and our management interviews. For example, the historical trends are of no value to us if the business lost its largest customer, one that comprised 90% of sales.

Business owners cannot increase their lifestyle—send their kids to expensive colleges, add a vacation home, and so on—based on the normalized income level. Before business owners can put cash into their pocket, they need to consider the following:

· What will be Uncle Sam’s cut of the profits?

· What big items need to be purchased to sustain operations?

· How much should be set aside to fund the growth of the business?

After paying taxes and setting aside funds to make major purchases and meet working capital needs, business owners can make cash distribution and do what they want with the funds.

How Sure Am I That It Will Go into My Pocket?

After the future sustainable cash flow is determined, it is important to determine the confidence level that a buyer would have in obtaining this cash flow. If buyers are very confident that it will land in their pocket, then they are willing to pay more for the business. If they are worried that the cash flow will not be there in three years, then they will not pay as much.

Valuators go through a process to determine what the proper rate of return should be for the business they are valuing, which includes looking at the specific risks associated with the business. This process will be explained more in the next chapter, and it is just as critical as determining the future sustainable cash flow. Small differences in this rate will make a significant difference in value.

The rate of return can only be determined by fully understanding the company’s risk profile and prospects for future growth. This is done by studying the industry and interviewing management. It is critical that the valuator truly understands all the risks associated with the business being valued.

![]() The Key Valuation Concept in Plain English How much can I put into my pocket by buying this business, and how sure am I that it will go into my pocket?

The Key Valuation Concept in Plain English How much can I put into my pocket by buying this business, and how sure am I that it will go into my pocket?

Besides knowing the answers to these two questions—how much and how certain—the answer to one additional question will determine the total price a buyer will pay for the business and the total proceeds the seller will obtain. This last question to ask is this: what am I buying? The business operations only, the enterprise value? Or the stock of the company, which includes the enterprise value?

Examples in Plain English

The best way to ensure that you fully understand the concepts presented in this chapter is by walking you through a simple example.

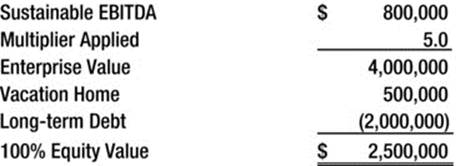

Scenario: Charlie is the 100% owner of a company that manufactures footballs, Fantastic Footballs, Inc., and he wants to sell his business. He has found a buyer and agreed to sell the business operations but not the stock of the company. The buyer and seller have agreed that the future sustainable EBITDA will be $800,000. They have agreed to use a multiplier of 5 of the estimated sustainable EBITDA to determine the enterprise value. The business owns a vacation home that is valued at $500,000, and it has a long-term bank debt of $2 million. The buyer does not want the vacation home and will not be paying off the debt at closing.

Enterprise Value Example

The enterprise value is the value of the company’s operating assets (intangibles, fixed assets, and working capital). In this example, the buyer has agreed to pay 5 times EBTIDA for these operating assets. The enterprise value of the company is calculated here:

Since it is an asset deal, the company will obtain a check for $4 million at closing. After closing, the assets of Fantastic Footballs will be a cash of $4 million and a vacation home of $500,000. The only remaining obligation is the bank debt of $2 million. What is the value of the company’s equity?

100% Equity Value Example

Charlie is excited that he sold his business for a good price and is comfortable about how the new owner will operate the business. He is anxious to invest the proceeds of the sale with his investment advisor. Since he sold only the operating assets of the business, the value of Charlie’s equity is determined by adding back the nonoperating assets and subtracting the value of the liabilities that are not part of the enterprise value. The equity value of the business is calculated here:

Charlie is surprised to learn that his equity value is not the 5 times EBITDA. In his retirement calculations, he assumed that he would have $4 million before taxes. He did not realize in the beginning of the selling process that the buyer would not be paying off his long-term debt. He needs to deduct the bank debt to determine how much he would realize after the sale and after he liquidates his company. But wait, there is one more surprise. Charlie must take one more step before he can spend or invest the money from the sale of his business.

Net Proceeds Example

Charlie’s retirement plan is to travel the world and spoil his grandkids. He thought that $4 million was enough to do this. Charlie’s stock is valued at $2.5 million after including the vacation home and the bank debt. Is this the amount that Charlie can give his investment advisor? No, it is not. Before he is able to spend or invest his sales proceeds, he must pay the tax man and the people that helped him sell his business.

Professional fees for a business transaction can include a success fee paid to an M&A intermediary or a business broker and fees paid to lawyers and accountants. In the following example, we will assume that the professional fees associated with selling Charlie’s business totaled $250,000.

Of course, you would expect that Uncle Sam wants to get a piece of the action. There are tax consequences in selling a business. The taxes paid depend on whether it is an asset sale or a stock sale and how the transaction is characterized in the purchase agreement. We will assume that the total tax paid on this transaction was $750,000. Fantastic Footballs is a C-Corporation and the tax includes a corporate tax on the sale proceeds over and above the company’s asset tax basis. In addition, Charlie must pay a tax on an individual basis after he liquidates the business to get his proceeds. We will explain the tax consequences of selling a business further in Chapter 5.

Charlie’s net proceeds from this deal after paying the transaction costs and the IRS are calculated here:

Charlie is not happy. He thought he was going to walk away with $4 million, but he instead is only getting $1.5 million!

![]() Important It is critical that you know the difference between enterprise value, equity value, and net proceeds.

Important It is critical that you know the difference between enterprise value, equity value, and net proceeds.

Summary

Hopefully after reading this chapter, you have a better understanding of the business valuation process. It is more complicated than simply putting numbers into a spreadsheet—but is less complicated than brain surgery.

As a business owner, it is vital that you understand the difference between enterprise value, equity value, and the net proceeds that you will receive after selling your business. Also it is important to know the difference between investment value and fair market value.

Now that you have a basic understanding on how a business is valued, let’s move on to show more details about the valuation process. In the next chapter, we will explain further how your business is valued using the income, asset, and market approaches to value.

All materials on the site are licensed Creative Commons Attribution-Sharealike 3.0 Unported CC BY-SA 3.0 & GNU Free Documentation License (GFDL)

If you are the copyright holder of any material contained on our site and intend to remove it, please contact our site administrator for approval.

© 2016-2026 All site design rights belong to S.Y.A.