Valuing and Selling Your Business: A Quick Guide to Cashing In (2014)

Chapter 5. Selling Your Business

Who Will Get Your Baby?

“Bruce, this is the last client that I will act as an intermediary for in selling a business.” I wish I would have said that one project earlier.

In 1999, my partner and I decided to expand our consulting practice to include the service of selling businesses for a success fee. The majority of our fees were based on whether we successfully located a buyer for our clients’ businesses.

The experience that I gained providing this service was invaluable and has enabled me to provide better advice to business owners about how buyers value their business and the selling process. This is because of the experience in dealing with the realities of the marketplace, I now advise my clients from “real-world” experience instead of a merely academic point of view.

We closed many deals, and it was a high-risk, high-reward service offering. When a business sold and the seller received the price that he wanted, everyone was happy and we got paid a lucrative fee. Other times, we spent a significant amount of time and resources on a deal that was never consummated and we did not receive a success fee. Most of the time, deals did not close because we did not find the right buyer willing to pay the price the seller wanted. Other times, we found the right buyer at the right price, but the sellers backed away at the last minute because they were not emotionally ready to sell. When we sold a business, we obtained a fee that was significantly higher than a consulting fee based on our hourly rates. Of course, if a deal did not close, the opposite happened. The feast-or-famine fee arrangement was frustrating in that it provided unpredictable income.

I knew providing this service was risky. When people buy a business for millions and it doesn’t work out the way they hoped, they like to point fingers. Usually, they don’t point their fingers at their own decisions.

When I reluctantly agreed to take on the engagement, I did not realize it was going to be part of my life for seven years and that I would be a defendant in a lawsuit for the first time in my life.

The lawsuit was settled a couple of years ago, so it is very fresh in my mind. We were sued three years and eleven months after the deal closed. The statute of limitations for professional services in Ohio is four years. Because of a confidentiality agreement, I cannot provide you with specific details of the engagement, but I will give you with an overview and describe the crux of the case.

The company that we represented was in the housing industry and was very successful. The deal closed in the winter of 2007, only a couple of weeks before the collapse of the housing market. The sellers that we represented started a similar type of business in the western part of the United States and decided they wanted sell their business and focus on their new companies.

The engagement started about one year before closing. We received a letter of intent (LOI) from the eventual buyer within weeks of being engaged by the sellers. Once the LOI was accepted, the buyer proceeded to perform due diligence over the next 60 days. The due diligence process did not go very well. The buyer came back and said he found many things that caused him concern and would agree to buy our client’s company at a significantly reduced price. My client was not too thrilled with the reduction in price, and we tabled the deal for a few months. A few months later, we reopened negotiations and the parties eventually agreed on a price. The attorneys then went to work on an asset purchase agreement and after a few hiccups, the deal eventually closed.

Within 90 days of the deal closing, the sellers were informed by the buyer’s attorney that they had violated the clause in the asset purchase agreement about providing accurate financial statements. The sellers provided financial data for a four-year period as an exhibit in the asset purchase agreement. The buyer claimed that one number was materially wrong on the latest financial statement provided. These statements were prepared by the sellers’ internal accountant and were not reviewed or audited by an outside accountant. We made it clear to the buyer that we did not provide any assurance about their financial records and that the buyer needed to conduct his own due diligence. The buyer hired a financial expert to examine the company’s financial records.

The buyers sued the seller to recover the monies held in escrow and demanded a good portion of the purchase price back. After a couple of years of battle, the sellers declared bankruptcy. The housing industry collapsed, and the epicenter of the collapse was the location where the sellers started their new business and invested the funds from the sale. Their personal fortunes were gone. During the lawsuit against our client, our records were subpoenaed and I was deposed. After it was clear that nothing could be recovered from the sellers, the buyer proceeded to sue us to recover his claims of damages. The discovery period lasted almost two years, including a dozen depositions in five different states. It was a very time consuming and emotionally draining process. Fortunately, I had a great support system with my family, friends and fellow partners at Rea & Associates—for which I am forever grateful.

My intention is not to scare you off from selling your business. I was involved with many deals that went very well and where both the buyer and seller achieved their goals, including those where the seller received tens of millions of dollars. It is very fulfilling to be part of the process that assists business owners in selling their business to the right buyer, enabling them move on to the next phase in life.

Selling your business will be one of the most difficult things that you will ever do. It is complex and time-consuming and will be hard on you emotionally. The perspectives that you will receive in this chapter come from both the “thrill of victory” related to successful deals and the “agony of defeat” regarding the ones that did not go so well.

There are two important decisions that you need to make preliminary to selling your business. The first is, “When is the best time to sell the business?” The second is, “Who is the best buyer?” The next two sections discuss these two decisions before turning to the “ins and outs” of the selling process.

The Best Time to Sell Your Business

The majority of business owners will eventually sell their business. Few will give it away to family members or simply shut down the business when they exit. With this in mind, when is the best time to sell your business? If the following is all lined up perfectly, you will be able to sell your business at the optimal price:

· Your sustainable cash flow has peaked.

· Your business risks are at the lowest level.

· Your forecasted growth is at its highest level.

· Bankers are lending money freely at great interest rates.

· The overall economy is doing well.

· Income taxes on business transactions are favorable.

· There are buyers available that have significant cash levels.

· There is aggressive buying of companies in your industry.

· You are able to find fulfillment and sense of purpose outside the business.

If all these factors are aligned perfectly for you today and you want out, don’t hesitate. Place your business on the market and reap your rewards!

But it’s not as easy as it seems. I have seen everything aligned perfectly for an industry only once in my career. This was in the late 1990s for the technology industry. The economy was humming, the infancy of the Internet was driving growth and profits to record levels, and there were irrational buyers in the marketplace. Companies were buying others based on multiples of revenues and not profits. The sellers were becoming millionaires though their companies had never achieved a profit. Then someone woke up and questioned the valuations of all the technology companies. The stock market crashed, and the economy slowed down. Timing is an important consideration when selling your business.

You cannot always predict swings in the market, and some factors are beyond your control in optimizing the timing for selling your business. These factors include current macroeconomic conditions, interest rates, industry trends, and buyer activity. Selling a business isn’t just about trying to time the market—it’s about timing your business.

You should therefore be diligent at all times in growing your business value and not be so worried about the general economic factors outside of your control. If you do this, then you can try to time the market to optimize your price.

This constant state of readiness also allows you to obtain a better price for your business should an unfortunate circumstance such as illness enter your life that forces you to sell the business sooner than you desired. There are other reasons why you may want to sell your business sooner than later. If you hate going to work everyday and are completely burnt out, it is time to get out—if only because you will not be able to focus on increasing the value of your business and may make serious mistakes that detract from its value. Alternatively, if you have reason to expect that over the next few years your earnings will decrease significantly due to circumstances out of your control, you may want to consider “cashing out” sooner than later.

![]() Important Concentrate on growing the value of your business while understanding how outside factors impact the best time to sell your business. This will allow you to maximize the price you will receive for your business.

Important Concentrate on growing the value of your business while understanding how outside factors impact the best time to sell your business. This will allow you to maximize the price you will receive for your business.

The Best Buyer for Your Business

Now to the question of who is the preferred buyer? There are two broad categories of buyers of businesses: synergistic and financial. Synergistic buyers are larger companies (usually competitors) in your industry and will pay you more for your business because they can achieve higher cash flows than you can through cost reductions (layoffs of employees) or increased margins. The financial buyer will continue the business in its present form. A financial buyer can be someone inside your business, a family member, or an outside investor.

You will have to decide whether obtaining top dollar for your business or continuing your legacy is more important. You rarely accomplish both of these goals with one buyer. Once you choose which type of buyer is the best for you, a strategy can be developed to find the right buyer. The following is a summary of the types of buyers and tips for selecting the best buyer for your business.

Selling to a Synergistic Buyer

Although the synergistic buyer option will provide the highest price, the number of synergistic buyers is limited and this option is not available to all business owners. You will want to consider selling to a synergistic buyer if you are in one of the following situations:

· Obtaining the highest price is most important to you: Many start a business to become rich. This strategy will provide the highest selling price for you. If you are concerned about your legacy or the future of your employees, then another option may be better.

· You have a retirement shortfall: You may not like the idea of selling to a competitor or other synergistic buyer, but it may be the only way to meet your retirement needs.

· The price received would provide a windfall that secures your family for life: I have been involved in deals where the business owner obtains tens of millions of dollars. They are able to provide financial security for their entire family for life and support charities they love. You may want your children to take your business, but it is hard to pass up an offer that secures your children’s financial future and allows them to pursue other endeavors.

Selling to an ESOP

An employee stock ownership plan (ESOP) is a qualified retirement plan for the employees of a company.1 If you sell your stock to an ESOP, it probably will be at a lower price than selling it to a synergistic buyer. However, you could end up with more after-tax proceeds. This is because you will have the opportunity to defer paying taxes from the gain of the sale of your stock to an ESOP. In order for this to happen, the proceeds must be reinvested in certain domestic investments (see IRS section 1042 for specifics). ESOPs are not easy to establish and can be costly to maintain. They are only possible if you have a strong management team that is able to operate your business once you leave. You will want to consider selling your stock to an ESOP if you are in one of the following situations:

· You desire to preserve the culture once you leave: This is a good option if you want to preserve both jobs and the culture you created. Outside buyers will run the business as they wish and may make changes you will not like. By selling it to your employees, it is more likely that your philosophy and legacy will continue than if you sell it to outsiders.

· You want to reward your employees: Some business owners sell their business to an ESOP because they appreciate all the efforts their employees have made to their success and want to reward them with ownership.

Selling to a Financial Buyer

Most business transactions are to a financial buyer that is not part of the business. There is a large universe of financial buyers, but they are hard to identify. Financial buyers can range from private equity groups to local corporate executives who have lost their jobs. They may be experienced buyers or complete novices. You will want to consider this option when the following apply to your situation:

· A synergistic buyer is not available: If you cannot attract a synergistic buyer and do not want to pursue an ESOP, then this option will provide you with the highest price. This is particularly true if there is competition among financial buyers for your business.

· You do not want a synergistic buyer: You may wish to preserve your culture and maintain jobs, but selling to family members or employees is not an option. Try to locate a financial buyer that has similar values and philosophy. If this is important to you, spend considerable amount of time with the buyer to make sure he or she is the right person to continue your legacy once you leave.

Selling to an Insider

Selling to your children, other family members, and/or key employees will provide you with the lowest amount of cash at closing compared with the other selling options. Most of the time, your children and employees will not have the financial resources needed to buy a business. Therefore, the amount of cash received at closing will be less than other options and you will have to finance a large part of the purchase price. Consider this strategy if the following is important to you:

· Your children own the business but not as a gift: You don’t need the money but want your kids to buy the business as a matter of principle. You may believe it is better for their children’s character that they have to buy the business with their own resources, or it is a fairness issue with your other children.

· You want an insider to own the business, but you do not have enough for your retirement: Some parents sell the business to their children because they need the sale proceeds to retire. Consider this option if you want an insider to own the business, but you need more resources to retire.

· You would like to continue to show up to work: If you sell the business to insiders, they may let you keep the keys to the front door and even ask you for your advice. When you sell it to an unrelated party, the new owners probably will make you turn in your keys, shake your hand, and wish you the best of luck.

You have spent a lot of blood, sweat, and tears in starting and operating your business. It is not an easy process of turning over the keys of your baby to someone else. It is important that you understand the advantages and disadvantages of each of these buyers and make a decision as to which type of buyer you would like to pursue.

Discuss these options with your spouse, kids, and trusted advisors. Each buyer type requires a different strategy and focus. For example, if you want to sell to an ESOP, you will have to have a strong management team; whereas a synergistic buyer might have key employees who will move into your business once the transaction is complete.

The Terms of the Deal

Selling a business is unlike any transaction that you have ever experienced. The largest transaction that most people have been involved with is real estate. Selling your house can be complex, but it is child’s play compared with selling a business. The price and cash you receive from selling your house are easy to comprehend. There is a closing statement that spells it all out. Also, it is clear what is being sold: your house and specific contents that have been identified in the simple three-page real estate contract. The same cannot be said about a business transaction.

When you sell your business, you will come to an agreement on the price for the business with the buyer. The next question to ask is this—how will the price be paid? It is rare when it is similar to a real estate purchase in that 100% of the price is paid at closing. The typical components of thepayment for a business include the following:

· The majority of the price is paid in cash at closing.

· A portion of the price is held in escrow.

· The seller may finance a portion of the deal by accepting a note from the buyer.

· The price may increase due to an earn-out clause.

· A consulting, noncompete and employment agreement is often included.

As a seller of your business, you want as much of the deal price as possible to be in cash at closing. The buyer wants the amount of cash paid at closing to be as little as possible. The amount paid at closing is part of the deal negotiations.

It is typical that a portion of the deal price will be placed in escrow to allow for a reduction in the price after closing for either a violation of the purchase agreement or buying an asset in which value is in question (e.g., the true value of accounts receivable). The amount placed in escrow is typically 10% to 20% of the purchase price for a 90- to 180-day period. The funds are held by an independent escrow agent and will be released to the seller once the buyer gives the escrow agent approval to release the funds.

Most buyers like the seller to have some “skin in the game” after they sell the business and to remain financially attached to the deal. This can be accomplished by a seller’s note, an earn-out and a covenant not to compete.

· Seller’s note: Many times, the seller will have to finance part of the purchase price. Buyers may need to bridge the gap between the purchase price and their own resources and the amount the bank will lend on the deal. The note covers the difference. The seller’s note is subordinate to bank financing, and you should always try to secure the note to a buyer’s reachable asset. I warn my clients to have the mindset that they may not collect the entire value of the note; thus, they should make all their financial plans based on cash received at closing. The note should not exceed 20% of the purchase price.

· Earn-out: An earn-out is the portion of the purchase price that is paid after closing based on reaching certain milestones previously agreed upon. This means the ultimate purchase price can increase if the buyer meets the goals spelled out in the earn-out. An earn-out is used when there is a valuation gap that needs to be bridged or when there is a large risk factor that concerns the buyer. For example, in Chapter 2, we discussed the client that had 90% of its revenues from one customer. A possible earn-out in that scenario is that a large portion of the purchase price is contingent on that main customer remaining for a specified time period.

Often, the buyer and seller cannot come to an agreement on the ultimate purchase price, but they would like to move forward. An earn-out gives sellers the ability to achieve the price they want and provides buyers some assurance that they have not overpaid. Performance-based earn-outs may be based on revenues, gross profits, EBITDA, or net income. I prefer that earn-outs be based on revenues or gross profits since the EBITDA and net income levels are subject to manipulation by the buyer. Early in my career, I was an expert in a litigation case where the buyer and seller had an earn-out arrangement based on the EBITDA levels. The seller never collected on that earn-out because the buyer proceeded to take out a $1 million salary and there were no profits left in the company to pay the earn-out.

· Covenant not to compete: In the majority of business deals, the seller is required to sign a covenant, as part of the transaction, not to compete. Most buyers would never buy a business if the seller could collect cash at closing and open up a competing business across the street. There usually is a separate value assigned to the covenant promising not to compete and is considered part of the total deal package. In addition, the seller may receive either a consulting agreement or an employment agreement as part of the deal. The buyer will want the seller’s expertise to assist in the transition process. Sometimes, this is included in the purchase price, and other times it is a separate contract signed at closing. Buyers like to shift some of the purchase price to a consulting agreement for tax purposes

What Are You Selling?

The answer to this question seems to be simple: your business! But it’s not that simple. Will you be selling your company’s stock or business assets? Will all of the business assets transfer to the buyer or just the goodwill, inventory, and equipment? Which party is responsible for the company’s liabilities? These questions will be answered during the negotiation process and documented in the purchase agreement.

As a seller, you will want to sell your company’s stock (stock deal) because you will then relieve yourself from any obligations that may arise from the past. Plus, there is a huge tax advantage. However, the buyer typically does not want to buy your stock but would rather buy business assets and assume as few of your liabilities as possible (asset deal). During my career, about 95% of sales transactions have been asset deals.

In a stock deal, the shares of stock of the business are transferred from the seller to the buyer, as well as all of the assets, liabilities, and operations. Also, any skeletons that may arise from the past (i.e., tax issues, product warranty, employee suits) will be the buyer’s responsibility. There are major tax disadvantages for the buyer in a stock deal. The business assets depreciate in the same manner as they did before the transaction, but at a rate that is lower than it would be under an asset deal. Also, the buyer is not able to write off any of the purchase price as a tax deduction. In a stock transaction, the buyer assumes more risks and has a significant tax disadvantage. It is rare when you find a buyer who is willing to do that.

In an asset deal, the seller retains ownership of the stock of the company. The buyer must either create a new entity or use another existing entity for the transaction. Only assets and liabilities that are specifically identified in the purchase agreement are transferred to the buyer. Other than some specified liabilities, such as accounts payables and lease obligations, all other liabilities of the company remain with the seller. This means if a lawsuit arises from an event prior to the closing of the deal, sellers will have to defend themselves out of their own funds. After selling the business under an asset deal, the seller liquidates the business entity and then receives the proceeds personally. Buyers record the assets and liabilities at the fair market value assigned to them as part of the transaction. This allows buyers to have greater annual depreciation of the fixed assets purchased, which lowers their income taxes. Unlike a stock transaction, the buyer will be able to write off any value assigned to goodwill as well as any other intangible assets over a 15-year period.

The seller’s tax consequence under an asset deal is usually much higher than under a stock deal. Sometimes the difference is significant. Because of the importance of this topic, we will discuss this further with an example at the end of this chapter.

The Steps in Selling Your Business

The process of selling your business is more complex, emotionally draining, and time consuming than selling a house. It is important that you are mentally ready for the uncertainty and stress that goes along with it. Have a timeline in your mind for when you would like to sell your business, but be flexible. Find someone you can trust who has either been through the process or has assisted others that you can talk with confidentially and openly while you are selling your business.

The following is the typical order of events that occur once you decide to place your business on the market:

· Select your transaction team.

· Locate the buyer.

· Sign a letter of intent.

· Enter the due diligence process.

· Negotiate the asset purchase agreement.

· Close the deal.

Before placing your business on the market, you want to be able to articulate your reasons for selling and you should also consider telling your key employees.

Many owners are reluctant to tell their key employees that they are selling the business. They fear these employees will run out the door searching for a new job if they hear that the business is for sale. One client told me that his biggest concern about placing his business on the market was that his employees would find out. He and his wife were 80 years old and frail. But actually, the employees were scared he would not sell the business and that it would be liquidated after his death.

I believe that it’s important that you inform your key employees of your intentions. They will likely sense that something is going on. Rumor and innuendo can make them leave faster than hearing the truth. Articulate why you are selling, assure them that you will tell the buyer how important they are to the business, and properly incentivize them to stay. The incentive that is popular in this situation is a large retention bonus that is paid to the employee(s) after the deal is closed.

Can you state your reasons for selling? Prospective buyers will want to know your reasons. Planned retirement or wanting to cash out and accept a new challenge in your life are some of the best reasons for selling. This provides some comfort to the buyer that there are no hidden business reasons for selling the business. Whatever the reason, make sure you can confidently explain it since buyers naturally wonder—if the business is so great, why are you selling?

![]() Important Keep the end in mind during the selling process. You are exiting for a reason so don’t let your emotions derail you from your financial and personal goals. Find someone you can trust during the process to be a sounding board and provide you with an objective perspective.

Important Keep the end in mind during the selling process. You are exiting for a reason so don’t let your emotions derail you from your financial and personal goals. Find someone you can trust during the process to be a sounding board and provide you with an objective perspective.

Select Your Transaction Team

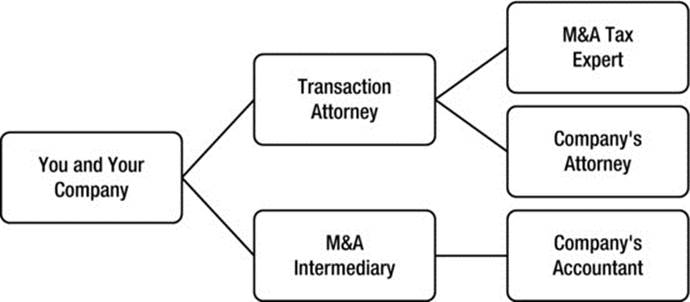

It is important that you select the right advisors to be on your team. Once the deal is closed, there is no turning back. For most, this will be the largest and most complex transaction that they will be a part of in their lifetime. You will need trusted, experienced advisors to assist you and be able to provide you with their full attention. Figure 5-1 shows which advisors are needed and how they interact with each other:

Figure 5-1. These experts are needed for an M&A transaction to allow the best chance for success

Before placing your business on the market, obtain an independent valuation that provides you with a value both for an investment value standard (synergistic buyer) and a fair market value standard (financial buyer). This valuation will provide you with some assurance of the validity of the offers you receive. You want someone independent providing you with the valuation and not the intermediary whose compensation is tied to the sale of the business.

The person whom you hire to find the buyer and quarterback the process has many different names in the business community, including investment banker, business broker, and intermediary. Investment bankers typically handle very large transactions (in excess of $100 million), whereasbusiness brokers deal with smaller transactions ($1 million or less). M&A intermediaries handle transactions in the middle, though both brokers and investment bankers sometimes dip into this territory as well. Throughout this chapter, I am going to use the term intermediary to mean the advisor who will quarterback the process. The intermediary receives a retainer or a commitment fee to initiate the selling process and will also receive a success fee if a transaction consummates, and they will want an exclusive arrangement for 6 to 12 months.

The intermediary has many different roles in the selling process. His main job is to find the right buyer for you, quarterback the entire process, and be the buffer zone between you and the buyer. It is a critical role. You want this person to create competition among buyers to drive up the price in a confidential way. Intermediaries need excellent communication and problem-solving skills and the patience of a marriage counselor. After obtaining an LOI, the intermediary will work closely with you and your accountant in the due diligence process. When you move to the purchase agreement, they will work in conjunction with the transaction attorney to make sure the agreement aligns with your wishes.

Hiring an intermediary is a good idea when you don’t know who the buyer may be or if there are a number of known potential buyers. If you don’t need someone to assist you in locating buyers and you know who the buyer of your business will be, then an experienced valuation professional or a CPA may be sufficient to assist you through the selling process. One of the most important roles of a professional assisting you in the selling process is to serve as a buffer between you and the buyer. Buyers want to have their questions answered and be able to express their concerns about the business to someone. This does not make for good conversation with the seller. I have seen many deals go sour because the seller had direct conversations with the buyer.

The transaction attorney has an equally important role: to let you sleep at night after the deal is closed. Studies have shown that less than 50% of buyers are satisfied with an M&A transaction. There are various reasons why so many are dissatisfied—they may believe they paid too much for the business or that they did not fully understand how the business operated. They may also feel that they were misled by the seller regarding the health of the business.

Even if you disclosed everything possible and the buyer had complete access to all materials, there is still a chance that the buyer will try to negotiate a lower purchase price or try to recover some of the proceeds paid to you. The transaction attorney’s role is to document your wishes in the purchase agreement and to limit your exposure to future litigation or recovery of funds once the deal has closed. They will work closely with your corporate attorney to ensure all legal issues have been disclosed. They also will work with the M&A tax expert to ensure the purchase agreement properly documents the tax treatment of the transaction. If the IRS ever questions the tax treatment of the deal, they will use the signed purchase agreement as the starting point in their investigation.

Finally, you will want to retain an expert in the M&A tax field. You need someone who really understands M&A tax issues and has years of experience. As you will see later in this chapter, a mistake in how taxes are treated in an M&A transaction can cost you dearly.

Remind your advisors that they work for you. Deals can get derailed if attorneys and other professionals have their egos hurt during the M&A process. When it gets nasty, they could easily lose sight of their client’s goal.

![]() Critical Make sure that the professionals on your team understand their role and that their job is to accomplish your ultimate goal—a successful sale. You are the one in control of this process.

Critical Make sure that the professionals on your team understand their role and that their job is to accomplish your ultimate goal—a successful sale. You are the one in control of this process.

Locate the Buyer

Once you choose which type of buyer is the best for you, you can develop a strategy to find the right buyer. If the buyer is outside of your company, you should work closely with the intermediary on developing this strategy. If you know that the buyer is an internal buyer, there is no need to hire an intermediary.

The intermediary will develop a marketing plan and send out a “teaser” about your business to develop interest. The teaser should not disclose your identity and should be discrete. Make sure that you review what is being sent out about your company to potential buyers.

Hopefully, the intermediary will have a robust response to this initial marketing campaign. The intermediary should screen potential buyers before providing them with any additional information. The screening process includes making sure the buyer is financially sound. Nothing is more frustrating than to spend months on a deal and find out that the buyer is not able to close the transaction due to lack of funds. You may want to screen out specific companies or individuals to whom you don’t feel comfortable giving access to your financial information. This could be your biggest competitor or someone who bought your friend’s company and did not keep his promises.

Once you are confident that the potential buyer has adequate financing and you feel comfortable with releasing financial information about your company, the prospective buyer should sign a confidentiality agreement. It is important that your corporate attorney reviews the confidentiality agreement to make sure it protects you. After the buyer signs the confidentiality agreement, the intermediary will send the buyer a confidential information memorandum (CIM). This document not only discloses your identity but includes a summary about your operations, historical financial results, and your prospects for the future.

The purpose of the CIM is to obtain an offer from a prospective buyer. Hopefully, you will have several offers to choose from and you will receive an LOI that meets your satisfaction.

![]() Suggestion “Date” the buyer before making any commitments. Spend a lot of time with the buyer to make sure this is the right person to take over your baby.

Suggestion “Date” the buyer before making any commitments. Spend a lot of time with the buyer to make sure this is the right person to take over your baby.

Sign a Letter of Intent

Once a buyer is found, it is time for the engagement period. The prospective groom gives his future bride the promise of a great life and his commitment with a ring. A buyer does the same thing with the term sheet or the LOI. Term sheets and LOIs are both preliminary, nonbinding documents that record an agreement between the parties on the major terms of a deal. The difference between the two is simply a matter of style. A term sheet lists the deal terms in bullet-point format, and an LOI is written in letter form. I will use the latter term in this chapter. These key components are a part of this agreement:

· Specifics of what is being purchased, including whether the transaction is an asset or stock deal

· Price and final pay-out at closing

· Agreement about any seller financing or earn-out

· Details of the due diligence process

· Removal of the seller from the market

· Proposal for a closing date

After you sign the LOI, you lose your negotiating power. The price and terms you agreed to in the LOI will not get any better and can become less favorable. During the due diligence process, if buyers find items they do not like, they may try to renegotiate the deal. I have never seen a case where the buyer says, “The business is better than we expected so we are going to offer you more money!”

For a specified period of time, you will have to honor a “no shop” agreement and take your business off the market. However, you don’t want the trail to get too cold if there are other interested parties. You need to limit the due diligence process and have the “no shop” agreement become void immediately if the buyer intends to materially change any deal terms. Give buyers a specific time period (less than 60 days) to perform their financial due diligence. I advise sellers to have a meeting with the buyer within 30 days of starting the due diligence process to determine if the buyer has any intention of changing the terms.

![]() Land mine Don’t sign an LOI until your attorney has reviewed it and you are completely satisfied with all deal terms. The deal will not get any better, and you can lose out on other interested parties if you sign an LOI with a buyer who will not honor the terms.

Land mine Don’t sign an LOI until your attorney has reviewed it and you are completely satisfied with all deal terms. The deal will not get any better, and you can lose out on other interested parties if you sign an LOI with a buyer who will not honor the terms.

Enter the Due Diligence Process

This is the most dreaded part of the deal process for the seller and intermediary. They have spent a significant amount of time and energy finding the right buyer and negotiating the LOI, and now someone is going to examine the business with a fine-toothed comb. It is the halfway point, and this is where most deals crumble. The seller will be inundated with questions and requests, all without knowing how the process is going from the buyer’s point of view. I have included a sample due diligence request (see Appendix C) in order to provide you with a general idea of what may be requested from you.

It is very important to disclose potential issues and less favorable items to the buyer prior to signing the LOI. It is much easier to negotiate the impact of any bad news on the deal price before signing the LOI rather than after signing it.

Most buyers will ask for a period of 60 to 90 days to complete their due diligence. Negotiate this down to no more than 60 days with a due diligence update midway through the process. Having audited financial statements available will make this process go much smoother and quicker. From the buyer’s perspective, the quality of information available about your business is critical. If the buyer is not confident that the company’s financial statements reflect reality, the deal will die or be subject to a price revision.

Most buyers will hire experienced CPAs and attorneys to go through the financial and legal records. CPAs will look at the quality of historical earnings and make sure that they are sustainable into the future. They will also examine critical areas such as receivable and inventory values, revenue recognition practices, and tax compliance. Typically, they will issue a written report to the buyer. The attorneys will search for potential legal, employee, and environmental issues and examine critical contracts and intellectual property protection.

Make sure that you involve your corporate attorney during this process. You don’t have to provide everything the buyer requests. You may not want to turn over your customer list or your secret formulas during this process. Seek the advice of your attorney if the buyer asks for anything that makes you uncomfortable.

If the buyer informs you that items were found in the due diligence process that will impact the terms of the deal, ask for their findings in writing. Take these findings to your advisors to determine their validity and what impact they will have on value.

![]() Due Diligence Tip Have a cooperative tone throughout the process and make it easy for the buyer to obtain the requested item. It raises suspicion if you are belligerent and do not respond properly to a valid request.

Due Diligence Tip Have a cooperative tone throughout the process and make it easy for the buyer to obtain the requested item. It raises suspicion if you are belligerent and do not respond properly to a valid request.

Negotiate the Asset Purchase Agreement

The Asset Purchase Agreement (APA) is the definitive agreement that finalizes all terms and conditions related to the sale of your company’s assets. It is different from a Stock Purchase Agreement, where the stock is sold including all assets and liabilities. Since a wide majority of deals are asset purchases, we will focus only on the APA. Generally, an APA contains the following items:

· The identification of the specific assets being purchased

· The purchase price

· The amount of cash to be paid at closing

· The details of any seller notes or earn-out

· What assets are excluded from the sale

· What liabilities will be assumed by the purchaser

· The date of closing

· Representations, warranties, and indemnifications

· The allocation of purchase price for tax purposes

· Exhibits that include financial statements

We have discussed most of these items. The exception is the representations, warranties, and indemnifications. It is important that you have an understanding of the purpose of these items in the APA. This is the area where the transaction attorneys earn their fee.

Representations and warranties are statements of fact and assurances made by both the buyer and the seller. Buyers want comprehensive representations and warranties to protect themselves against any problems or unforeseen issues. Sellers want to give as few representations and warranties as they can and limit the financial impact if there is a breach. Indemnification provides one party with a contractual remedy for recovering post-closing monetary damages arising from a breach of a representation, warranty, or any other contract issue.

In the deal that I opened the chapter with, the buyer asserted that there was a breach in the seller’s representation about the accuracy of the financial statements. The remedy they sought (indemnification) was the release of the escrow funds to their account and an additional payment by the seller to reduce the price paid. When my client refused these conditions, the buyer sued the seller.

Representations, warranties, and indemnification terms are the focus of a substantial amount of time and energy in negotiations. The only way to avoid this is to agree with all of the buyer’s wishes in this area and have a significant portion of your proceeds from the sale held in escrow. However, this approach is not something I would recommend.

As a seller, your goal is to provide reasonable representations and warranties and limit your indemnification exposure. You can place caps on the damage amount, as well as time limits when damages can be claimed. Different areas of exposure may require different time limits. A financial statement representation may expire after one year, but an environmental representation may last much longer.

![]() Land mine Don’t minimize the importance of the representations and warranty promises that you make in the APA and understanding the indemnification clause. Don’t sign the APA until you are confident that you will not end up in court post-closing.

Land mine Don’t minimize the importance of the representations and warranty promises that you make in the APA and understanding the indemnification clause. Don’t sign the APA until you are confident that you will not end up in court post-closing.

Close the Deal

This is what you have been waiting for. Sign the APA and get your money! However, most deals do not close upon the signing of the APA, and there can be a small time lag to make sure that the transition from old owner to new owner is smooth. The deal is not closed until you see the funds wired into your account or a check at the closing table. At closing, you will have some deductions from your sale proceeds. Intermediaries receive their fee at closing and other professionals that assisted in the transaction may also insist on being paid at closing. There are no taxes withheld at the closing, and you will need to send what you owe to the IRS based on the recommendations of your tax advisor.

Funds that are held in escrow will be sent to an escrow agent and are released based on the terms in the APA. If buyers make a claim on the escrow funds, they will ask the seller to tell the escrow agent to release the disputed funds to them. At times, there is litigation over the escrow funds. It is important that your APA is very clear about how escrow is released and how disputes are resolved.

The Tax Impact of a Sales Transaction

The saying “don’t let the tail wag the dog” applies to the area of taxes on M&A transactions. Taxes are a very important consideration when selling your business but don’t let the tax issue drive your decision-making process. Too many business owners fret over taxes rather than growing the value of their business. To retire rich, grow your business. Then when you are ready to sell, hire an M&A tax expert to minimize the impact of taxes on the transaction.

The seller and the buyer have competing interest when it comes to taxes on a deal. Typically, what is good for the seller is not beneficial to the buyer. This is why your tax expert should be brought in early in the process and not at the end of the deal.

In this section, I do not intend to make you a tax expert on M&A transactions. Frankly, this area is too complex for me, and I rely on tax experts in my firm for all M&A transactions. The point I want to make is how important it is to have a tax expert assist you through a transaction. To emphasize this, it’s helpful to look at best- and worst-case illustrations.

Each different legal form of business (C corporation, S corporation, LLC, and partnership) has different rules in regards to M&A transactions. Regardless of the legal form of business, the gains on a transaction are either classified as ordinary income or a capital gain. The tax rate difference between ordinary income and capital gains is significant, and there are specific rules from the IRS for what classifies as ordinary income vs. a capital gain.

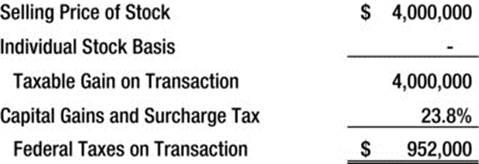

In order to understand the tax consequences on a sales transaction, I will continue with the example of Fantastic Footballs, Inc. At the end of the last chapter, Charlie’s business was worth close to $4 million and we will assume that he receives an offer of $4 million. The two examples that follow demonstrate the difference between a stock sale and an asset sale.

With these calculations, I will assume the highest 2014 tax rates (ignoring the impact of state and local income taxes) and that Fantasy Footballs is a C corporation. For a stock deal, sellers recognize a gain based on the difference between the sales price and their current basis in the stock. Basis is the owner’s original investment. If you did not buy your business, the basis of your stock is usually minimal. For this example, Charlie’s stock basis is zero. The gain is taxed at the capital gains rate along with the new Medicare surcharge tax on investment income. The federal income tax calculation for the stock transaction is shown here:

Charlie will have to pay $952,000 in federal income taxes. That’s a lot of money. However, it gets worse under an asset deal.

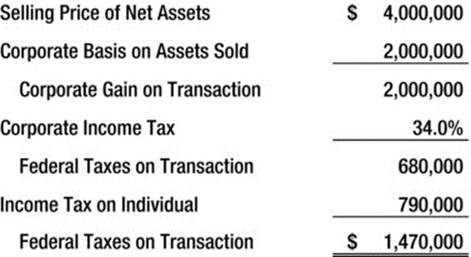

Now let’s look at the tax treatment of an asset deal. There is one additional assumption that we need to add. Each asset that a company owns has a tax basis, which is usually the asset’s original cost less any depreciation. We will assume that the tax basis of the assets being sold is $2 million. The company receives a check for $4 million and will have a $2 million taxable gain on the transaction. The company has to pay taxes on the difference between the selling price of the assets and the amount on which the assets are recorded on the books for tax purposes (tax basis). After paying the corporate tax on the transaction, business owners then have to pay taxes on the amount that is sent to them personally after the transaction is closed.

In this example, the company owes $680,000 in taxes from reporting a gain on the sale of the assets. The only asset that Fantastic Footballs has now is $3.32 million in cash. Charlie liquidates the company and receives the $3.32 million as a dividend, and he has to pay taxes on that amount at the individual level. Based on the 2013 tax law, Charlie’s federal tax rate on this distribution will be 23.8% (dividend rate and Medicare surcharge on investment income). He will owe $790,000 individually on this distribution. The combined corporation and individual tax from the transaction is $1.47 million.

The difference in the income tax bite between an asset deal and the stock deal is huge! It is $518,000. Now this is the worst-case scenario. If Charlie hired a good tax expert, there are legitimate strategies to lower the tax bite of the asset deal.

![]() Tip The basic rule of thumb in M&A transaction is to have as much of the taxable gain classified as a capital gain rather than ordinary income. If the buyer will not allow a stock deal, have your tax advisor show you areas where you can achieve capital gains rates on an asset deal.

Tip The basic rule of thumb in M&A transaction is to have as much of the taxable gain classified as a capital gain rather than ordinary income. If the buyer will not allow a stock deal, have your tax advisor show you areas where you can achieve capital gains rates on an asset deal.

Other business entity forms (besides a C corporation) do not have to worry about the double taxation issue (except some S corporations that were once C corporations), but there is still a battle over what is classified as a capital gain and ordinary income.

Both the buyer and the seller will have to include Form 8594 to report the sale to the IRS. On this form, the total selling price of the business is allocated to the various asset classes transferred in the sale. The values entered on the seller’s and buyer’s copy of Form 8594 must be identical.

My Top Ten Tips in Selling a Business

To end this chapter, here are my top ten tips when it comes to selling your business:

1. Don’t wait too long. Exit your business from a position of strength, not weakness. It is important to sell before you become bored with the business, or worse yet, an illness or retirement forces a sale.

2. Have a reasonable expectation on the price that you desire for your business. Since an inflated figure either turns off or slows down potential buyers, rely on a valuation expert to help you arrive at what your company is truly worth. Do not set a price for your business. Instead, have buyers provide you with a price that they are willing to pay. They may surprise you with a price higher than your expectations or true value.

3. Don’t let taxes drive your actions but don’t neglect their impact.

4. Engage a team of experienced M&A professionals. This is the best way to obtain the highest selling price, minimize your tax burden, and allow you to sleep at night after the deal is closed.

5. Prepare for the sale years in advance. This includes having audited or reviewed statements at your disposal from years back and updating important legal documents.

6. Achieve a higher price through buyer competition. Hire the right intermediary who can create a competitive situation with buyers. The more buyers bidding for your business, the higher price you will obtain.

7. Be flexible. Don’t be the kind of seller who wants all cash at the closing, who won’t accept any contingent payments, or who insists on a stock transaction.

8. Disclose potential negative factors early. Make sure that there are no unpleasant surprises for the buyer during the due diligence process. This will save you time and money and avoid killing a deal or renegotiating a price at a lower value.

9. Don’t let time drag down the deal. To keep up momentum, work with your advisors to be sure the buyer adheres to a strict time schedule.

10.The line from an old song is true for the M&A process: “You got to know when to hold ‘em, know when to fold ‘em.” If the market or your gut is telling you that this is not the right time to sell after starting the process, pull the plug, reassess, and start the process again when the time is right.

Summary

The most popular exit strategy is the sale of a business. The majority of business owners will eventually sell their business, and it’s most likely going to be the largest and most difficult transaction in their lifetime. It’s not the time for saving fees by using inexperienced professionals or going through this process alone. The amount received on the sale of your business will impact your financial future.

M&A activity ebbs and flows. It is important that you are ready to enter the market at the right time. The best time to sell is when your business and M&A activity are strong. It is important to have your business in a saleable position in order take advantage of peaks in the market.

Make sure that you have the right professionals on your team. You will need an experienced intermediary, tax professional, and a transaction attorney. Each one has a critical role to play, but always remember that you are the one who is in charge of the process. Do not ignore the impact on income taxes when you sell your business. You can lose 50% of the purchase price to income taxes with an improperly structured deal.

_______________

1It is not in the scope of this book to fully explain what ESOPs are and the advantages and disadvantages of them. For further information please visit http://www.nceo.org/

All materials on the site are licensed Creative Commons Attribution-Sharealike 3.0 Unported CC BY-SA 3.0 & GNU Free Documentation License (GFDL)

If you are the copyright holder of any material contained on our site and intend to remove it, please contact our site administrator for approval.

© 2016-2026 All site design rights belong to S.Y.A.