University Startups and Spin-Offs: Guide for Entrepreneurs in Academia (2015)

Part I. Strategies for University Startup Entrepreneurs

Chapter 8. The Financial Model

Although researchers are generally comfortable talking about their technology and its features at length, they are often much less well-versed in the business and financial aspects of their undertaking. Entrepreneurs need to be in a position to answer a few key financial questions about their venture. What are we producing that has a value in the market? Will the market pay us enough to be profitable? How exactly are we transferring money from customers into our bank account? The business-model canvas answers the first question, but the other ones require a financial model made with spreadsheet software.

When you sit across the table from venture capitalists, they will grill you about your financial model. You should know the size of your potential market, your expected market share, how long you believe it will take you to sell a product in this market, and how you plan to turn your market share into profit for your company. If you cannot answer a few basic financial questions, no one will take you seriously as a startup entrepreneur.

That being said, there is one thing investors know with certainty about your financial model: the model will be wrong. Investors are well aware of that, so they want to see the assumptions that underlie your forecast, much more than the forecast itself. Putting together your financial model will give you an impression of the time it will take for your startup to achieve some level of profitability. You will also have worked out your own overhead and capital needs, often called the burn rate. All this is what investors look at, not the hockey-stick revenue-growth chart that all other startups have in their models as well. How you put together your financial model is more informative than the individual numbers.

Financial models and projections can be simple, but there are some pitfalls to avoid. I once made the mistake of proudly announcing that “If we sell widget X to 1% of the people in China for $1 each year, we will make $10 million in revenue.” The venture capitalist had of course heard this lame pitch many times before, and responded, “You expect just 1% market share? What kind of small-minded company is this? I only invest in companies with 80% market share.” With that, the discussion was over. A $10 million market seemed big for me at the time, but less so for anyone who has been in the business longer. A good market starts at about $100 million per year in sales revenue.

Basics of Financial Business Modeling

If you are already familiar with accounting and building financial models for startups, feel free to skip this chapter. If not, then here is a quick primer on the most important terms in a financial model. This is my personal approach, and I realize there are many different opinions about how to do it right. The procedure I explain in this chapter is one that I find workable without knowing much about corporate finance. It helps jumpstart the discussion about a startup’s finances without much spreadsheet programming. If you prefer another modeling technique, that’s fine. As long as you can explain what you are doing and why you are doing it, all roads lead to Rome.

The important terms in your financial model are revenue, cost, profit, and profit margin. Their formulas are as follows:

Revenue = number of units sold × price charged per unit

Cost = fixed cost + variable cost

= fixed cost + (number of units sold × cost per unit)

Profit = revenue - cost

Let’s look at each of these in a little more detail:

· Revenue means the total proceeds from sales. It is the money brought into the company by its business activities. You calculate this amount by multiplying the number of units sold by the price per unit. The term revenue is sometimes used interchangeably with sales, and the two mean the same thing. Many people confuse the revenue with profit. Even though your company may have $100 million in revenue per year, its profit may still be zero or negative.

· Profit is the money left in your account after you pay all costs incurred by the company. When calculating profit in your spreadsheet, also make a clear distinction between pre-tax profit and after-tax profit. Because taxes are a percentage of profit, you simply multiply the corporate tax rate by the pre-tax profit. Startup entrepreneurs often forget to make this distinction, but it can make a big difference, especially if your tax rate is high.

· The percentage of revenue that you keep as profit is called the profit margin. This number shows how profitable your company is. Because it is a ratio, you can use it to compare the profitability of different companies.

· Costs consist of fixed costs and variable costs. Fixed costs are the overhead of the company that stays the same regardless of the number of units sold. Rent paid for offices, support services, all salaries, and so on, are fixed costs. Variable costs change with the number of units sold. For example, if you are producing a car, then these include the metal, plastics, engine, tires, and so on. If you pay licensing fees for patents per car sold, then these fees are also part of the variable costs.

These are the most important terms. There are of course many more formulas in financial accounting, but these should be enough for a simple financial model for a startup. If you think accounting is exciting, then feel free to pick up any book on the subject to learn more.

It often takes entrepreneurs by surprise to hear that the most vital parts of their model are the costs and the assumptions that underlie the revenue projection. Revenue and profit projections in themselves are less important, because you cannot predict them accurately. Regardless, you should set up your business model so that your startup can achieve high revenues. If a company has high revenue, it can improve its profit by reducing fixed and variable costs, courtesy of economies of scale. Building 1 item results in a higher cost per item compared to producing 100 items. A bigger factory can often turn out a product at a lower cost than a small one.

When you begin building the financial model, first fill in the parts that you know already. These may be the fixed cost and variable cost per unit sold. You may have a validated assumption about the price charged per unit. With this, you already have half the model. The tricky part is the speculation about how many units you can sell each year. I discuss some guidelines for this later in this chapter.

How Investing in Startups Works

When investors give you money, they obviously expect something in return. Where does this return come from? Not from revenue, but from the profit your company makes in the future. With their money, investors buy a certain number of shares in your company. This number of shares, as a percentage of the total shares in the company, controls the percentage of profit each investor is entitled to receive.

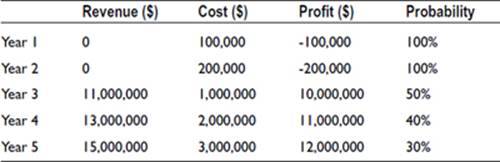

Let’s say you can make the case that your company will turn a profit of $10 million in year 3, $11 million in year 4, and $12 million in year 5, as shown in Table 8-1. Before year 3, profit was negative. This projection enables you to make a ballpark assumption about the value of your company today. There are many ways to arrive at such a value, and to explain them all here would be outside the scope of this book. A straightforward procedure to arrive at a speculative number for the value of your company is to discount the projected future cash flows by their probability and sum them up, as follows:

Company value = 1×(-$100,000)+1×(-$200,000)

+ 0.5×$10,000,000+0.4×$11,000,000+0.3×$12,000,000

= $12,700,000

Table 8-1. Projected Future Cash Flows

This is an example to illustrate how the numbers in your financial model work in context. Of course, it is an extreme simplification, and specialists in finance will cringe when they see me advocate this technique. Venture capitalists will look at your underlying assumptions and come up with a valuation of their own. As a quick hack, the probability method is workable without going back to school and learning about corporate finance. Most important, this number will put into perspective investment offers you may be receiving.

Let’s say you have arrived at the projections just outlined. The big jump in revenue in year 3 results from talks you had with a potential joint venture partner. He wrote you a letter of intent saying that if you can develop your technology to a certain point, he will be willing to form a joint venture with you. Because this partner is a leading multinational, you can expect better distribution channels, instant economies of scale, and larger projects. Your own costs will increase, but because your profit margin is high, you can reasonably expect high profits. Now a venture capitalist visits your startup and offers you $250,000 for 10% of the company. Does this sound like a good deal? Let’s see: if 10% of your company cost $250,000, then 100% are worth $2,500,000. The numbers you calculated paint a different picture: your company value at the current time is $12,700,000, so 10% equals $1,270,000. Based on your own numbers, you should expect a much better offer from the venture capitalist. According to your calculation, she should get roughly 2% equity in your company, not 10%, for her $250,000 investment.

With the assumptions gained in putting together your financial model, you can begin a negotiation without flying blind. The number you calculate as the present value for your company is either too high or too low. You need to check and update it often and get feedback from others about it. But now you see how your startup’s numbers work. They are not rocket science, but they also are not immediately obvious. An entrepreneur who has no clue about the value of his company will be taken advantage of by shrewd investors. Most of all, they will doubt he is genuine in his efforts if he comes across as financially illiterate. As soon as you can lead a qualified discussion about your financial model, investors will take you more seriously.

It is unnecessary to hire an MBA or a financial advisor to program the financial model for you. Much more important is that you understand the drivers and underlying assumptions of the model and what they mean for your business. You should be able to modify the model yourself.

A joint venture partner will often value your company differently than a venture capitalist—for example, in terms of costs the partner can save by buying your R&D, or in terms of the IP advantage gained over a competitor. Nevertheless, it is useful to have your own model at hand. Most likely you will need it only when you speak with investors or potential partners.

Identify Your Market

Previously I skipped the discussion of how to arrive at the number of units sold in your startup. Before I address this, you first need to understand the different kinds of markets. Author Steve Blank summarizes them in the following manner: 1

· Existing market: A new entrant is stealing a slice of a market. Users abandon competitor products when they start using yours. Instead of increasing the pie, you just take a slice.

· Re-segmented market: You increase the pie by selling to customers who otherwise would not buy at all—for example, by introducing a less-expensive product that adds price-conscious customers to the market.

· New market: Your technology is new, and by definition you own 100% of the market. You must explain to the market what the product is and how to use it. Customers will still use other products when they start using yours.

The most important thing to show in your financial model is what Steve Blank calls Product/Market Fit.2 Netscape founder Marc Andreessen describes this as “being in a good market with a product that can satisfy that market.”3 Most companies are re-segmenting markets in one way or another. A rule of thumb for achieving Product/Market Fit is that at least 40% of users should say they would be “very disappointed” without your product.4

What does this mean for your financial model? Most important, you need to demonstrate that you can sell to at least 40% of the market. If yours is an existing market, then you can find out its size relatively easily courtesy of Google. Perhaps there is even a market study available. Or an academic paper or trade journal in your library. Or a footnote in the quarterly report of the industry leader.

Re-segmented markets are more complicated to assess, because you have to make some assumptions about the size of the slice you are adding. Calculate several scenarios, starting from 10% up to 50%. In either case, your projected annual revenue should land somewhere around $100 million and upward. As I said before, investors know that this number is mostly fiction, but it should be achievable with your startup if everything goes well.

Let’s forget about new markets for now, because they are rare and the most speculative to assess.

The number-one thing not to do is to conjure up hockey-stick growth, where in the first years you have no sales, and then, magically, in year 3 the business takes off like a rocket, doubling or tripling its income year after year. If you have real commitments, like the joint venture discussed in the example of company value, then your financial projections are much stronger, and you can explain the underlying assumptions for hockey-stick growth. But if you cannot, then the hockey stick will look silly. Future revenue projections are not all that important. What counts is a strong business model that harvests demand today and in the next few years from existing markets. At the end of the day, everything else is fiction. Unless you have a classic business model, such as a real-estate investment with a large sunk cost of several hundred million and rental revenue over the next 20 years, projections into the future make little sense. For a tech or hardware startup in the early stages, they are little more than wishful thinking. Just show the size of the market, the share you aim to achieve eventually, and how your pricing strategy fits into that equation.

When you know the market size and your market share, then you have to fit that around your pricing model for your product or service. Many eye openers along the way will show you either that you need to charge an enormous sum for your product or that your market is simply too small to allow you explosive growth. When that is the case, you can use this new insight in your future MVP testing. Look for other products and services, and other markets, and test those. Your costs may also be too high to let your startup achieve profitability, in which case you need to reduce them. The lean canvas and the financial model are like sparring partners that can help you do so.

The Story Matters More Than the Numbers

Every serious investor knows that financial projections for a startup are rarely going to come true, so you must prepare to answer questions about the underlying assumptions that led to your projections. Don’t get me wrong: you still need the financial model; it is an essential tool to help you form useful assumptions about your market, your business model, and your strategy. But it is key to be clear about the story that explains how the financial model came about. How did you discover the market your product is serving? How did you come up with the market share your company is aiming to achieve? Can you make a credible case about exactly how your company will turn a profit? How did you arrive at the timeline? All this information is more helpful for investors than an upward-sloping revenue curve. They will form their own opinion of you as an entrepreneur and combine that with their assumptions about the product and the market. If they see that you are smart and have come up with a good idea to commercialize a certain technology with profit, they will be more likely to invest in you. The financial model will be the platform on which this discussion takes place.

Make sure the output of the model fits on one page, where you also explain all the underlying assumptions. With this and the lean canvas, you will have condensed your entire business proposition onto a few sheets of paper. When you meet with investors or potential partners, present your business with both the business-model canvas and the financial model. See what they gravitate toward and what they remark. Then incorporate those new findings into the next version of your documents.

These are the basics you should be familiar with when building financial models. If you have heard enough about finance and economics, feel free to skip the rest of this chapter. Otherwise, read on to see how economic theory is not all that useful in startup entrepreneurship.

A Word about Economic Theory

As you already learned, becoming an expert in economics or corporate finance is unnecessary to create your financial model. More often than not, it may even be a disadvantage. It is good to know some basics of economics, because they are helpful for explaining things in hindsight. But when you are putting together your financial model, it is better to be blissfully ignorant. Let’s find out why.

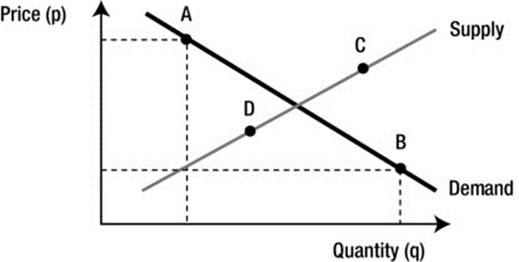

The discipline of modern economics is a strange conglomeration of sociology, psychology, and philosophy. On the basic level, it splits into two main sections: microeconomics and macroeconomics. The former concerns itself with the theory of individual firms and addresses supply and demand for products, price theory, market structures, and so on. Macroeconomics applies itself to the workings of all companies together in an economy as a whole, and the interrelationships with other economies. How the size of a company affects its production costs is a matter of microeconomics, whereas the amount of money in circulation and the effect on a country’s GDP is part of macroeconomics. When talking about individual companies, we are operating in the domain of microeconomics. The most basic model in this discipline is the so-called supply-and-demand model, which you may be familiar with from Economics 101 (see Figure 8-1).

Figure 8-1. Classical supply and demand model

What does this model express? Look at the demand curve first. This shows how much of a product people buy in relationship to its price. When the price of a product is high, such as at point A, the quantity demanded is low. Fewer people are able to afford the high price, or people may be unwilling to pay more than a certain amount for a certain product. At point B, the price is low, and the quantity of products demanded is higher. This is assumed to be the case because people can buy more of the good with $100 when the price is low than when the price is high.

The supply curve works in a similar way. This curve shows the relationship of price and quantity supplied from the manufacturer’s point of view. How much of a certain product does the company produce and make available in the market in relationship to the price it can charge? Assume the price is high, such as at point C. The supplier has an incentive to flood the market with product, because the company has the potential to make much more profit when it sells the product at a high price. But when the price is low, as at point D, the supplier is not interested in producing much, because overall profit is lower in a low-price environment. At the point where the supply curve and the demand curve intersect, the market is in equilibrium.

This is the story of the supply-and-demand model. Does it make sense to you? Most likely it does. But let’s look at an example that flies in the face of this neat model and relegates it straight to the garbage bin.

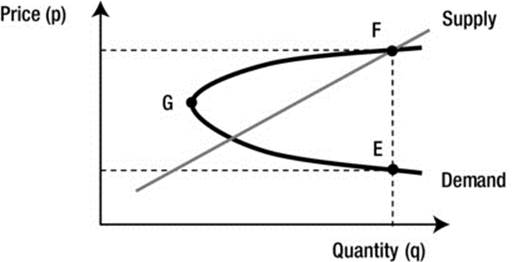

In the last decade, there was a huge boom in real-estate prices. Many investors doubled their investment with real-estate speculation in the United States, China, and other parts of the world. When prices were low, real estate was not that attractive, because most people could not imagine that a sizable return would ever come to pass. But when things picked up and prices soared, more and more people became interested in real estate and began speculating. Demand increased as soon as prices increased. Is this what the supply-and-demand model would predict? No—quite the opposite. Figure 8-2 shows how the real-estate boom looks in the supply-and-demand model.

Figure 8-2. Supply-and-demand model in a real-estate boom

There are now two possible prices for each quantity. One is in the low-price environment, where those with little money can purchase a house (E). When prices go up, fewer of those people can afford a house, and demand declines. Then comes an inflection point (G), where rising prices spur a real-estate boom and speculative buying. This designates the beginning of the high-price environment. Everybody who can piles into real estate, and demand increases. More and more speculators are attracted to the market. They buy second and third homes. Demand goes up, and prices go up in tandem (F). In such a market, do high prices lead to fewer or more units sold? It depends. There may be fewer units sold in a low-price environment, but more units sold in a high-price environment. You will not find this supply-and-demand model in an introductory economics book, but you may have witnessed the dynamics of a real-estate boom firsthand. Would you say the classical supply-and-demand model is useful to analyze such a boom, or other transactions in the real economy? In this light, probably not. It would lead you to the wrong assumptions and might cost you a lot of money. Uncertainty and complexity have no place is most economic models.

This goes to show that economists hardly have all the answers, even though they like to think they do. If you hire an MBA or economist to work out your financial model, the danger is that they will tell you with much authority how this has to be done. More often than not, their knowledge is firmly rooted in theory, which has proven to be precisely wrong more than once in history. Much better than basing your financial model on economic theory is to look at the real numbers and comparable firms already active in the market. Pair this information with your own assumptions about the future, and make your own scenarios.

When I started my first company, I had no idea about economic theory. It felt intuitively right to charge the highest price possible for my services. And it was clear that I would have to decrease my overhead to increase my profit. I knew that I had to cold-call hundreds of potential clients in order to get a foot in the door. In your early 20s, you have many things on your mind other than cold-calling prospects. How I wanted to destroy that phone at times. Yet it was clear that there was no way around it, and the 189 remaining names on the list were a stark reminder. No slick business strategy could have saved me from doing the real work. Because I knew nobody who would bankroll my startup, hiring someone to do the dirty work was out of the picture. Like many other entrepreneurs, I had to make do with limited means. Knowledge of economic theory would have been nothing more than a distraction. It was unnecessary at the time.

Years later, when I actually studied economics at the London School of Economics, many “aha!” moments occurred. It was satisfying to know the theory to explain in hindsight why some of my businesses had worked and others had not. But I still find economic theory and business school knowledge to be of little use for startup entrepreneurs. This is true not only for the simplest of all models, the supply-and-demand model we just looked at. Porter’s Five Forces to formulate competitive strategy,5 Christensen’s Innovator’s Dilemma,6 and many other theoretical concepts are nice to know but by no means necessary for startup success. A business consultant for a multinational company may benefit from being familiar with some of these concepts, but startup entrepreneurs should focus on the tasks at hand with “build, measure, learn” and many other practical strategies explained in this book. If you are seriously interested in learning more about economics later down the road, then it may be worth looking into in more detail. But avoid distracting yourself in your first startup. Make all your brain power available for things that really matter.

Never Rely on Specialists

Some entrepreneurs are deeply averse to anything that has to do with finance or business modeling. They feel they should focus on the core of their technology and prefer that someone else handle the rest. Students and researchers are not immune to this. Somebody may suggest including an MBA student on the founding team to bring in expertise about running a company and leading interactions with the world outside the university. I think this is the wrong approach. It is like hiring somebody else to go on a holiday for you and report back to you in detail about their adventures while you sit on the couch at home. Startup entrepreneurship is a learning experience that encompasses disciplines outside of your domain. It is a mindset, not a job. With that mindset, you should embrace the opportunity to integrate new skills into your life. You may discover a talent that you never knew you had.

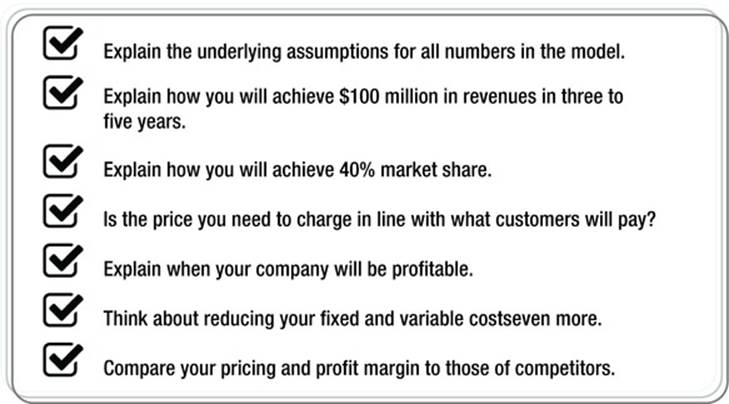

Luckily, the financial part of a startup is relatively small, so all you have to learn are the basic functions of Excel to put together your financial model. More than that is not necessary. Nobody expects you to know about depreciation schedules and the Double Irish with a Dutch Sandwich. Your tax accounting should be outsourced to an accountant. They can file your taxes for a few hundred dollars. But the financial model cannot be outsourced. It is one of the core building blocks of your company that the founders must understand. Each time new findings emerge, you should be able to adjust the financial model yourself. Handing this off will be a disadvantage for your startup. Figure 8-3 provides a recap for using financial models effectively.

Figure 8-3. Checklist for financial models

Sales and marketing are a similar story. Learning how to interact with others professionally will be a huge asset to you as an entrepreneur. Engaging third parties with a proposition that is in their own best interest applies to more than sales and marketing. Giving them actionable next steps to obtain the benefits of your product or service will be at the heart of your startup’s success. Forget the cliché of the vacuum salesman who shuffles from door to door trying to sell a gadget that nobody needs. Getting others to buy something is mostly a communication skill. It has little to do with spending millions of marketing dollars to push your product in front of clients. If they see no obvious benefit, they will not buy—it’s as simple as that.

Just as basic finance skills, communication skills need to be native to the startup’s original founders; they should not be purchased from an external source. As the saying goes, business has only two functions: marketing and innovation. Spend a few weeks learning the ropes yourself. Learn to lead engaging discussions with others, and you will lay the centerpiece for your startup success. Turning the discussion away from features to the benefits of a technology is the first step, and this is a skill best acquired by doing. An MBA (or any other degree) has very little to do with sales and marketing success, or business success in general. Make yourself a smart and likable person, and sales and marketing will become a natural communication process for you.

____________________

1Steven G. Blank, The Four Steps to the Epiphany: Successful Strategies for Products That Win (K&S Ranch, 2007).

2Steven G. Blank and Bob Dorf, The Startup Owner’s Manual: The Step-By-Step Guide for Building a Great Company (K&S Ranch, 2012).

3Marc Andreessen, “Product/Market Fit,” Stanford University, June 25, 2007, www.stanford.edu/class/ee204/ProductMarketFit.html.

4Brant Cooper and Patrick Vlaskovits, The Entrepreneur’s Guide to Customer Development: Cheat Sheet to The Four Steps to the Epiphany (Newport Beach, CA: Cooper-Vlaskovits, 2010).

5Michael E. Porter, Competitive Strategy: Techniques for Analyzing Industries and Competitors (New York: Free Press, 1980).

6Clayton M. Christensen, The Innovator’s Dilemma: When New Technologies Cause Great Firms to Fail (Boston: Harvard Business School Press, 1997).

All materials on the site are licensed Creative Commons Attribution-Sharealike 3.0 Unported CC BY-SA 3.0 & GNU Free Documentation License (GFDL)

If you are the copyright holder of any material contained on our site and intend to remove it, please contact our site administrator for approval.

© 2016-2026 All site design rights belong to S.Y.A.