QuickBooks 2017 All-In-One For Dummies (2016)

Book 2

Getting Ready to Use QuickBooks

Contents at a Glance

1. Chapter 1: Setting Up QuickBooks

1. Planning Your New QuickBooks System

2. Installing QuickBooks

3. Dealing with the Presetup Jitters

4. Running the QuickBooks Setup Wizard

5. Identifying the Starting Trial Balance

2. Chapter 2: Loading the Master File Lists

1. Setting Up the Chart of Accounts List

2. Setting Up the Item List

3. Working with the Price Level List

4. Using Sales Tax Codes

5. Setting Up a Payroll Item List

6. Setting Up Classes

7. Setting Up a Customer List

8. Setting Up the Vendor List

9. Setting Up a Fixed Assets List

10. Setting Up a Price Level List

11. Setting Up a Billing Rate Level List

12. Setting Up Your Employees

13. Setting Up an Other Names List

14. Setting Up the Profile Lists

3. Chapter 3: Fine-Tuning QuickBooks

1. Accessing the Preferences Settings

2. Setting the Accounting Preferences

3. Setting the Bills Preferences

4. Setting the Calendar Preferences

5. Setting the Checking Preferences

6. Changing the Desktop View

7. Setting Finance Charge Calculation Rules

8. Setting General Preferences

9. Controlling Integrated Applications

10. Controlling Inventory

11. Controlling How Jobs and Estimates Work

12. Dealing with Multiple Currencies

13. Starting Integrated Payment Processing

14. Controlling How Payroll Works

15. Telling QuickBooks How Reminders Should Work

16. Specifying Reports & Graphs Preferences

17. Setting Sales & Customers Preferences

18. Specifying How Sales Are Taxed

19. Setting the Search Preferences

20. Setting the Send Forms Preferences

21. Fine-Tuning the Service Connection

22. Controlling Spell Checking

23. Controlling How 1099 Tax Reporting Works

24. Setting Time & Expenses Preferences

Chapter 1

Setting Up QuickBooks

IN THIS CHAPTER

![]() Planning how you’ll use QuickBooks

Planning how you’ll use QuickBooks

![]() Installing the QuickBooks program

Installing the QuickBooks program

![]() Preparing for setup

Preparing for setup

![]() Setting up QuickBooks

Setting up QuickBooks

![]() Figuring out your starting trial balance

Figuring out your starting trial balance

To use QuickBooks, you need to do two things: Install the QuickBooks software and run either the Express Start or Advanced Setup version of the QuickBooks Setup process. This chapter gives you a bird’s-eye view of both of these tasks. I also want to spend just a few paragraphs talking about some of the planning that you should do before you set up QuickBooks and some of the missing setup steps in the QuickBooks Setup process — things it should do but doesn’t. (Don’t worry: I tell you how to complete the missing steps, partly at the end of this chapter and also in the next chapter.)

Planning Your New QuickBooks System

I start with a couple of big-picture discussions: what accounting does and what accounting systems do. If you understand this big-picture stuff from the very start, you’ll find that the QuickBooks Setup process makes a whole lot more sense.

What accounting does

Think about what accounting does. People may argue about the little details, but most would agree that accounting does the following four important things:

· Measures profits and losses

· Reports on the financial condition of a firm (its assets, liabilities, and net worth)

· Provides detailed records of the assets, liabilities, and owner’s equity accounts

· Supplies financial information to stakeholders, especially to management

What accounting systems do

Now take a brief look at what accounting systems, or at least at what small-business accounting systems typically do:

· Produce financial statements, including income statements, balance sheets, and other accounting reports.

· Generate business forms, including checks, paychecks, invoices, customer statements, and so forth.

· Keep detailed records of key accounts, including cash, accounts receivable (amounts that customers owe a firm), accounts payable (amounts that a firm owes its vendors), inventory items, fixed assets, and so on.

· Perform specialized information management functions. In the publishing industry, for example, book publishers often pay authors royalties. So royalty accounting is a task that book publishers’ accounting systems typically must do.

What QuickBooks does

Okay, after you understand what accounting does and what accounting systems typically do, you can see with some perspective what QuickBooks does:

· Produces financial statements

· Generates many common business forms, including checks, paychecks, customer invoices, customer statements, credit memos, and purchase orders

· Keeps detailed records of a handful of key accounts: cash, accounts receivable, accounts payable, and inventory in simple settings

Allow me to make an important observation here: QuickBooks does three of the four things that you would expect an accounting system to do. Compare the list that I just provided with the preceding list (“What accounting systems do ”). I’ll save you the time of finding the fourth thing: QuickBooks doesn’t supply the specialized accounting stuff. It doesn’t do royalty accounting, for example, as discussed in the earlier example.

And now for the bad news

So QuickBooks does three of the four things that accounting systems do, but it doesn’t do everything. QuickBooks is often an incomplete accounting solution. Be careful, therefore, about setting your expectations. Typically, you also need to figure out work-arounds for some of your special accounting requirements.

QuickBooks gives users and businesses a lot of flexibility. To return to the previous example, a book publisher can do much of what it needs to do for royalty accounting in QuickBooks. This royalty accounting work simply requires a certain amount of fiddling as the business is setting up QuickBooks.

But QuickBooks (or at least the most popular versions) does suffer a couple of significant weaknesses:

· QuickBooks Pro doesn’t supply a good way to handle the manufacturing of inventory. QuickBooks Premier and QuickBooks Enterprise Solutions do support simple manufacturing accounting, however, and QuickBooks Enterprise Solutions provides some additional inventory management capability (multiple inventory sites, lot and serial number tracking, and FIFO costing) as part of its Advance Inventory feature. These versions of QuickBooks help you account for the process of turning raw materials into finished goods and also deal with some real-life inventory complexities.

· Only QuickBooks Enterprise Solutions handles the situation of storing inventory in multiple locations. In other words, QuickBooks Pro and QuickBooks Premier simply show, for example, that you have 3,000 widgets. It doesn’t let you keep track of the fact that you have 1,000 widgets at the warehouse, 500 widgets at store A, and 1,500 widgets at store B.

In spite of the fact that QuickBooks may be an incomplete solution and may not handle inventory the way you want or need, QuickBooks is still a very good solution. No, wait — that’s not really strong enough. What QuickBooks does, it does very well.

Like a lot of things in life, finding the right accounting solution is all about balance. Some of the factors that you may consider when choosing your accounting software would be ease of use, portability, price, data security, customer service, and the way it integrates with other business tools. The desktop version of QuickBooks has been a good balance of the things I need, which is why I use it for my business.

The desktop version of QuickBooks provides considerably more horsepower than the online version of QuickBooks (or other cloud-based systems). That said, the online version makes it far easier to work with an outside accountant or bookkeeper. Accordingly, for those clients who really need outside professional help but who don’t need advanced desktop features (like job costing), the online version of QuickBooks is a very reasonable choice, too.

The desktop version of QuickBooks provides considerably more horsepower than the online version of QuickBooks (or other cloud-based systems). That said, the online version makes it far easier to work with an outside accountant or bookkeeper. Accordingly, for those clients who really need outside professional help but who don’t need advanced desktop features (like job costing), the online version of QuickBooks is a very reasonable choice, too.

Installing QuickBooks

You install QuickBooks the same way that you install most applications or programs — either by download or via a disc containing the software. I’d begin at https://quickbooks.intuit.com , where you can compare some of product options, chat with a sales agent, or, if you are ready, purchase the version of your choosing. After purchase, you should be able to download the product (definitely reach out to Intuit if you can’t). If you purchase a copy of QuickBooks from a brick-and-mortar store, you just need to insert the disc into the proper drive.

After downloading the program (or inserting the disc containing the software), you don’t need to do anything special to install QuickBooks. Simply follow the onscreen instructions. Typically, you’re prompted to enter the installation key or installation code. This code and key are available within the QuickBooks packaging — usually, on the back of the envelope that the disc comes in — if you purchase the software in a local store. Otherwise, Intuit provides these items to you during the online purchase.

The QuickBooks installation process may ask you to answer questions about how you want QuickBooks to be installed. Almost always, you want to accept the default suggestions. In other words, QuickBooks may ask you whether it can create a new folder in which to install the QuickBooks program files. In this case, choose yes.

If your version of Microsoft Windows doesn’t recognize that you’ve stuffed the QuickBooks CD into the machine’s CD or DVD drive, you have a couple of choices:

· You can wait. If you wait, Windows probably will recognize that you’ve placed the QuickBooks CD in the CD or DVD drive, and after a short wait (even though it may seem like an eternity), Windows starts the process of installing the QuickBooks program.

· You can manually force the installation of the QuickBooks program. Windows includes a tool that you can use to add or remove new programs (unsurprisingly named the Add/Remove Programs tool). I don’t describe how this Control Panel tool works here, but you can refer to a book such as Windows 10 For Dummies, by Andy Rathbone (John Wiley & Sons, Inc.), or Windows online Help to get this information. In a nutshell, you simply open the Control Panel window, click the Add/Remove Programs tool, and follow the onscreen instructions for telling Windows to install a program stored on the CD or DVD in the computer’s CD or DVD drive.

QuickBooks can work as a multiuser accounting system. This means that several people can use QuickBooks. The QuickBooks data file — the repository of all the QuickBooks information — typically resides on a centrally available computer or server. People who want to work with the QuickBooks data file simply install the QuickBooks program on their computers and then use the program to access centrally located QuickBooks data files. This multiuser system isn’t complicated to run; in fact, I talk about it quite a bit in Book 7, Chapter 1 .

QuickBooks can work as a multiuser accounting system. This means that several people can use QuickBooks. The QuickBooks data file — the repository of all the QuickBooks information — typically resides on a centrally available computer or server. People who want to work with the QuickBooks data file simply install the QuickBooks program on their computers and then use the program to access centrally located QuickBooks data files. This multiuser system isn’t complicated to run; in fact, I talk about it quite a bit in Book 7, Chapter 1 .

You need to own a separate copy of QuickBooks for each computer on which you install QuickBooks. You can also buy multiuser copies of QuickBooks that let you install the QuickBooks program on up to 5 computers (or on up to 30 computers if you’re running QuickBooks Enterprise Solutions). I mention this because you don’t want to get involved in software piracy — which is a felony — as part of inadvertently setting up QuickBooks in the wrong way. The bottom line: You need a legal copy of QuickBooks for every machine on which you install QuickBooks.

You need to own a separate copy of QuickBooks for each computer on which you install QuickBooks. You can also buy multiuser copies of QuickBooks that let you install the QuickBooks program on up to 5 computers (or on up to 30 computers if you’re running QuickBooks Enterprise Solutions). I mention this because you don’t want to get involved in software piracy — which is a felony — as part of inadvertently setting up QuickBooks in the wrong way. The bottom line: You need a legal copy of QuickBooks for every machine on which you install QuickBooks.

Dealing with the Presetup Jitters

After you install QuickBooks, you run an onscreen wizard to set up QuickBooks for your firm’s accounting. Cleverly, this onscreen wizard is called QuickBooks Setup. In the next sections, I explain what you need to do before you use the QuickBooks Setup so that you work in an efficient manner. I also give you an overview of what you’ll do as you go through the QuickBooks Setup.

Preparing for setup

In running QuickBooks Setup, you provide quite a bit of information to QuickBooks. As a practical matter, setup and postsetup cleanup (which I describe in this chapter and the next one) require that you have the following:

· Accurate financial statements as of the conversion-to-QuickBooks date

· Detailed records of your accounts payable, accounts receivable, inventory, and fixed assets

· A complete or nearly complete list of employees, customers, vendors, and inventory items (if you buy and sell inventory)

You want to get all this stuff together before you start QuickBooks Setup because (depending on how you go about setting up QuickBooks) you may be asked about this stuff as part of the setup process. Don’t try to scurry around looking for a particular piece of data while you’re running the setup wizard; collect this data up front. Then stack all the necessary paperwork on your desk next to your computer.

Let me also note that you’re going to make several accounting decisions as you go through QuickBooks Setup. You may be asked to decide whether you want to use an accounts payable system, for example. You may choose to use the setup wizard to tell QuickBooks whether you want to send customers monthly statements. You may also be asked whether you want to prepare estimates for customers or whether you want to use classes to further track your income and spending.

In general, when you’re asked any of the accounting questions, you can simply accept the default answer. You’re required by law to be consistent in your accounting for tax purposes, however. If you want to change your accounting — technically called a change of accounting method by the Internal Revenue Service — you must request permission from the IRS to make that change. How to do this and the ramifications of doing it are beyond the scope of this book, but be forewarned: The IRS insists that you be consistent in your accounting. If you’ve been treating particular items of income or expense in a certain way, the IRS says, “Hey, dude, you must continue to treat them that way unless you get permission from us to change.”

I should make a clarification: You can use one accounting method for your tax return and then, within QuickBooks, use a different accounting method. You may be locked into using accrual-basis accounting on your tax return, for example. But that doesn’t mean you can’t use cash-basis accounting within QuickBooks and in managing your business. Accordingly, what I say in the preceding paragraphs is a little bit inaccurate. Technically. But you probably don’t want to use one accounting approach on your tax return and a different approach in QuickBooks. Too complicated.

One final note: You should have your tax return from last year handy because it supplies information that you need for running QuickBooks Setup. Last year’s tax return, for example, supplies your taxpayer ID number, your legal business name, and your method of accounting.

Seeing what happens during setup

As you walk through the setup process, you work with QuickBooks to set QuickBooks preferences (which determine how QuickBooks works and which features are initially available) and to set up a chart of accounts and your bank accounts.

The chart of accounts, just so you know, identifies those income, expense, asset, liability, and owner’s equity accounts that appear in your financial statements.

After you complete QuickBooks Setup, you’re almost ready to begin using QuickBooks. In fact, in a pinch, you could (after QuickBooks Setup) limp along with QuickBooks.

An important point of clarification: You may think that you should be ready to rock and roll after installing QuickBooks and running through the setup. But you have two other tasks to complete: identifying your starting trial balance (which I describe at the end of this chapter) and loading your key master files (which I mostly describe in the next chapter). The trial balance identifies your year-to-date income and expense numbers, and your asset, liability, and owner’s equity numbers as of the conversion date. The master files store information about customers, vendors, employees, and inventory items that you repeatedly use. The customer master file, for example, stores a customer’s name and address, phone number, and the contact person’s name (if different).

Running the QuickBooks Setup Wizard

After you install the QuickBooks program, the installation program may start QuickBooks automatically and then start QuickBooks Setup. You can also start the QuickBooks Setup by starting the QuickBooks program the same way you start any program and by then choosing the File ⇒ New Company command to start QuickBooks Setup.

Getting the big welcome

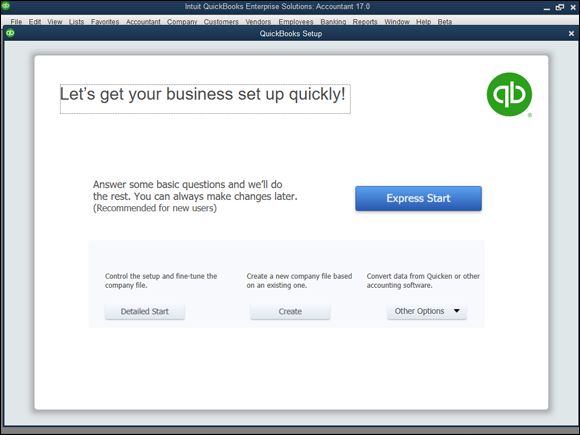

The Let’s Get Your Business Set Up Quickly screen of QuickBooks Setup (see Figure 1-1 ) appears when you choose File ⇒ New Company. The screen provides some general information about setting up a new company within QuickBooks. You probably want to read this screen’s information. When you’re ready to begin, click either the Express Start button or the Detailed Start button.

FIGURE 1-1: The QuickBooks Setup window, showing the welcome message.

The Express Start method

QuickBooks provides an accelerated version of the QuickBooks setup process, which you can use when you don’t want to customize setup. If you click the Express Start button, QuickBooks collects a bit of information about your company and, based on that information, sets up a company file that should work for a business like yours.

After you click Express Start to create the company file, QuickBooks prompts you to describe the people (customers, vendors, and employees) you do business with, the items you sell, and your bank account. You provide these descriptions by stepping through a series of screens and filling in onscreen boxes and worksheets. I describe how this process works later in the chapter, in the section “Adding your information to the company file .”

The Detailed Start method

The Detailed Start button, if clicked, starts the EasyStep Interview, which walks you through a bunch of screens full of information that let you rather tightly specify how the company file that QuickBooks sets up should look.

To move to the next screen in the EasyStep Interview, you click the Next button. To move to the previous screen, you click the Back button. If you get discouraged and want to give up, you can click the Leave button. But try not to get discouraged.

Supplying company information

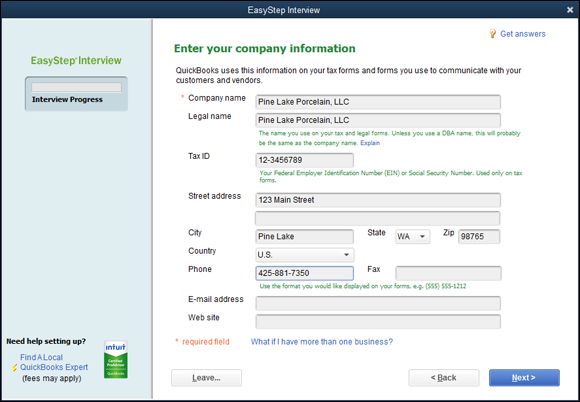

The first few screens of the EasyStep Interview collect several important pieces of general information about your business, including your company name and the firm’s legal name, your company address, the industry in which you operate, your federal tax ID number, the first month of the fiscal year (typically, January), the type of income tax form that your firm uses to report to the IRS, and the industry or type of company that you are operating (retail, service, and so forth). The first screen of the EasyStep Interview is shown in Figure 1-2 .

FIGURE 1-2: The first screen of the EasyStep Interview collects general company information.

QuickBooks isn’t very smart about the tax accounting rules for limited liability companies (LLCs). An LLC can be treated as a sole proprietorship if it has one owner and as a partnership if it has more than one owner. But LLCs may also elect to be treated as S corporations or C corporations. If you’ve made such an election for your LLC, be sure to indicate that the LLC is an S corporation or C corporation.

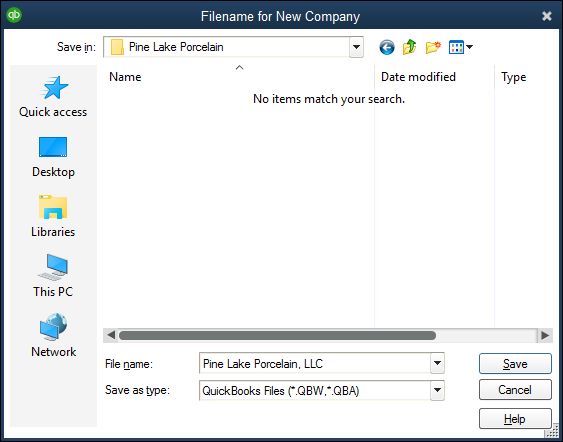

After collecting this general company information, QuickBooks creates the company data file that stores your firm’s financial information. QuickBooks suggests a default name or a QuickBooks data file based on the company name (see Figure 1-3 ). All you need to do is accept the suggested name and the suggested folder location (unless you want to save the data file in the Documents folder, which isn’t a bad idea).

FIGURE 1-3: The Filename for New Company dialog box.

Customizing QuickBooks

After QuickBooks collects the general company information mentioned in the preceding paragraphs, the EasyStep Interview asks you some very specific questions about how you run your business so it can set the QuickBooks preferences. Preferences in effect turn on or off various accounting features within QuickBooks, thereby controlling how QuickBooks works and looks. Here are the sorts of questions that the EasyStep Interview asks to set the QuickBooks preferences:

· Does your firm maintain inventory?

· Do you want to track the inventory that you buy and sell?

· Do you collect sales tax from your customers?

· Do you want to use sales orders to track customer orders and back orders?

· Do you want to use QuickBooks to help with your employee payroll?

· Do you need to track multiple currencies within QuickBooks because you deal with customers and vendors in other countries, and these people regularly have the audacity to pay or invoice you in a currency different from the one your country uses?

· Would you like to track the time that you or your employees spend on jobs or projects for customers?

· How do you want to handle bills and payments (enter the checks directly, or enter the bills first and the payments later)?

Setting your start date

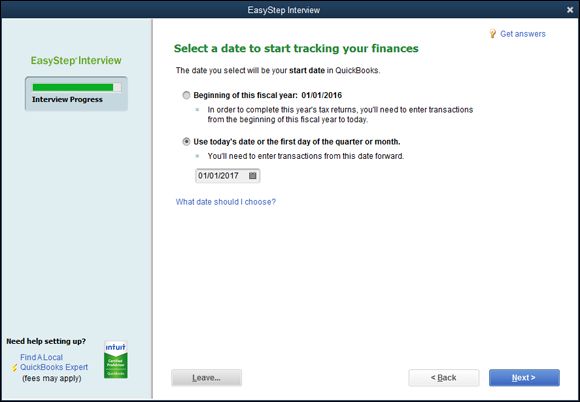

Perhaps the key decision that you make in setting up any accounting system is the day on which you begin using your new system. This day is called the conversion date. Typically, you want to begin using an accounting system on either the first day of the year or the first day of a new month. Accordingly, one other big question you’re asked is about the conversion date. You’re prompted to identify the start date by using the dialog box shown in Figure 1-4 .

FIGURE 1-4: The EasyStep Interview dialog box that lets you select the start date.

The easiest time to start using a new accounting system is the beginning of the year. The reason? You get to enter a simpler trial balance. At the start of the year, for example, you enter only asset, liability, and owner’s equity account balances.

At any other time, you also enter year-to-date income and year-to-date expense account balances. Typically, you have this year-to-date income and expense information available only at the start of the month. For this reason, the only other feasible start date that you can pick is the start of a month.

In this case, you get year-to-date income amounts through the end of the previous month from your previous accounting system. If you’ve been using Sage 50 Accounting, for example, get year-to-date income and expense amounts from Sage.

After you’ve provided the start date, supplied the basic company information, identified most of your accounting preferences, and identified the date on which you want to start using QuickBooks, you’re almost done.

If you click the Leave button, QuickBooks leaves you in the QuickBooks program, ready to get to work. The EasyStep Interview process isn’t lost forever, however. To get back into the interview, just open the file you were in the process of setting up. When you do, the EasyStep Interview restarts.

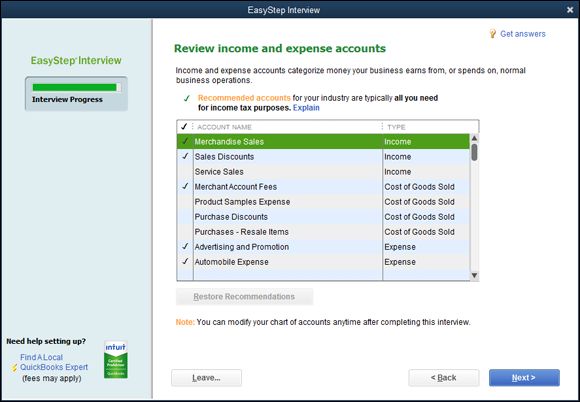

Reviewing the suggested chart of accounts

At the very end of the EasyStep Interview, based on the information that you supply about your type of industry and the tax return form that you file with the IRS, QuickBooks suggests a starting set of accounts, which accountants call a chart of accounts. These accounts are the categories that you use to track your income, expenses, assets, liabilities and owner’s equity. Figure 1-5 shows the screen that the EasyStep Interview displays for showing you these accounts.

FIGURE 1-5: The EasyStep Interview screen shows you its recommended income and expense accounts.

The accounts that QuickBooks marks with a check, as the screen explains, are the recommended accounts. If you don’t do anything else, these checked accounts are the ones you’ll use (at least to start) within QuickBooks. You can remove a suggested account by clicking the check mark. QuickBooks removes the check mark, which means that the account won’t be part of the final chart of accounts. You can also click an account to add a check mark and have the account included in the starting chart of accounts.

You can click the Restore Recommendations button at the bottom of the list to return to the initial recommended chart of accounts (if you made changes that you later decide you don’t want).

When the suggested chart of accounts looks okay to you, click Next. It’s fine to just accept what QuickBooks suggests because you can change the chart of accounts later.

Adding your information to the company file

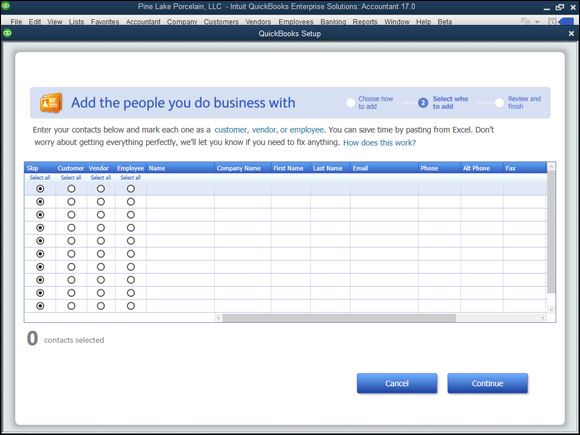

No matter whether you use the Express Start method of creating a company file or the Detailed Start/EasyStep Interview method, after you and QuickBooks set up the company file, QuickBooks prompts you to enter your own information in the company file (see Figure 1-6 ).

FIGURE 1-6: The QuickBooks Setup screen that prompts you to enter your own information in the company file.

Customers, vendors, and employees

To describe customers, vendors, and employees, click the first Add button. QuickBooks asks whether it’s possible to get this data from someplace else, such as an email program or email service (Outlook, Gmail, and so forth), or if you just want to enter the information into a worksheet manually. You’re probably going to enter the information manually, so click the appropriate button and then click Continue. When QuickBooks displays a worksheet window (see Figure 1-7 ), enter each customer, vendor, or employee in its own row, and be sure to include both the name and address information. Click Continue when you finish. QuickBooks then asks (using a screen I don’t show here) whether you want to enter opening balances (amounts you owe or are owed) for customers and vendors. Indicate that you do by clicking the Enter Opening Balances link and then enter the opening balances in the screen that QuickBooks provides.

FIGURE 1-7: The QuickBooks Setup screen that collects information about the people you do business with.

Services and inventory items you sell

To describe the stuff you sell, click the second Add button (refer to Figure 1-6 ). QuickBooks asks about the stuff you sell — whether you sell services, whether you sell inventory items, and whether you want to track any such inventory items you sell, for example. Answer these questions by clicking the option button that conforms to your situation and then click Continue. When QuickBooks displays a worksheet window (not shown), describe each item you sell on a separate worksheet row. Also be sure to describe any inventory items you’re holding at the time you convert to QuickBooks. Click Continue when you finish. If you sell more than one type of item, you need to repeat this process for each type of item.

Business bank accounts

To describe your business bank account (or bank accounts), click the third Add button (refer to Figure 1-6 ). When QuickBooks displays the Add Your Bank Accounts worksheet window (not shown), provide each bank account’s name, account number, and balance on the conversion date. When you finish entering this information, click Continue.

Identifying the Starting Trial Balance

Regardless of whether you use the Express Start version or the Detailed Start/EasyStep Interview version of the QuickBooks Setup process, you don’t actually get a complete trial balance in the QuickBooks company file simply by setting up. Assuming that you follow the instructions and tips provided in the preceding paragraphs, you get only your bank account, accounts receivable, inventory, and accounts payable balances in QuickBooks. Yet you need to enter all the missing trial balance information in QuickBooks, too, to begin getting good reports out of QuickBooks and to use the software for supplying financial data to your tax returns. I end this chapter by talking about how you get the rest of the trial balance data into the QuickBooks company file.

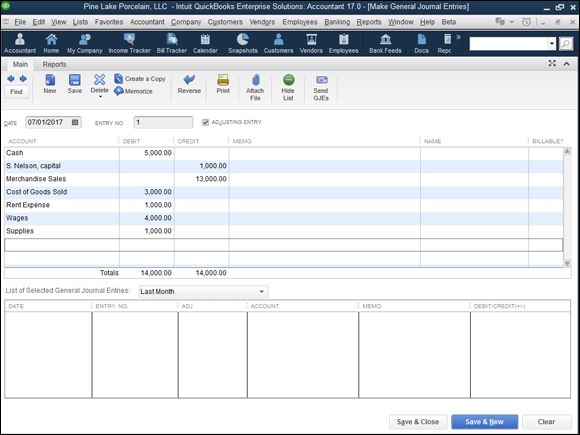

A simple example to start

To record the rest of your starting trial balance, you record a journal entry. The journal entry records the remaining trial balance amounts for all your other accounts at the conversion or start date: accounts other than your bank accounts, accounts receivable, accounts payable, and inventory.

As a simple example to show you how this works, suppose that you have the trial balance shown in Table 1-1 . Note that these trial balances are used in the discussion in Book 1, Chapter 2 and shown in that chapter’s Table 2-19 . Please notice that no balance is recorded for a bank account, no balance is recorded for accounts receivable (because this account doesn’t even show up in the trial balance), and no balances are recorded for inventory or accounts payable (because these accounts have zero balances at the conversion date). For purposes of this example (but not the next example), the cash balance isn’t a bank account but is actually cash: a desk drawer full of low-denomination, used bills with nonsequential serial numbers.

TABLE 1-1 A Trial Balance

|

Account |

Debit |

Credit |

|

Cash |

$5,000 |

|

|

Inventory |

0 |

|

|

Accounts payable |

$0 |

|

|

S. Nelson, capital |

1,000 |

|

|

Merchandise sales |

13,000 |

|

|

Cost of goods sold |

3,000 |

|

|

Rent expense |

1,000 |

|

|

Wages |

4,000 |

|

|

Supplies |

1,000 |

|

|

Totals |

$14,000 |

$14,000 |

Figure 1-8 shows how the Make General Journal Entries window looks when it records the missing trial balance information from Table 1-1 . After this journal entry is recorded, the trial balance is correct as of the start date.

FIGURE 1-8: The Make General Journal Entries window, showing a simple trial balance.

For more information about how to record a journal entry by using the Make General Journal Entries window, see Book 4, Chapter 1 . If you want to try this on your own with no further instruction from me, choose the Company ⇒ Make General Journal Entries command. When QuickBooks displays the Make General Journal Entries window, as shown in Figure 1-8 , use the Account, Debit, and Credit columns to record your journal entry.

If the idea of making a journal entry terrifies the heck out of you, you may find yourself in a bit of a pickle. You need to become comfortable working with double-entry bookkeeping to set up QuickBooks at a time other than at the beginning of the year. This means, unfortunately, that if you’re setting up QuickBooks sometime during the middle of the year, you must enter a general journal entry to fix the weirdness that the QuickBooks Setup creates. If you don’t know how double-entry bookkeeping works — if debits and credits aren’t your friends — you probably need to get somebody’s help. I suggest that you call your CPA or some other friend who truly understands accounting. Get him or her to come over and enter the last part of the trial balance for you by using the Make General Journal Entry window.

Note: This shouldn’t be a big project if you decide to call your CPA. If she comes over to your office, and if you have the trial balance ready for her, it should take her only a few minutes to enter the necessary general journal entry. Perhaps you can buy her a nice lunch, and that will settle the score.

A real-life example to finish

Okay, true confessions. The example I give in the preceding section? You probably won’t be lucky enough to have your starting trial balance journal entry be so simple. You probably will have to deal with a bank account and with account balances in your accounts receivable, accounts payable, or inventory accounts. Now I show you how this works.

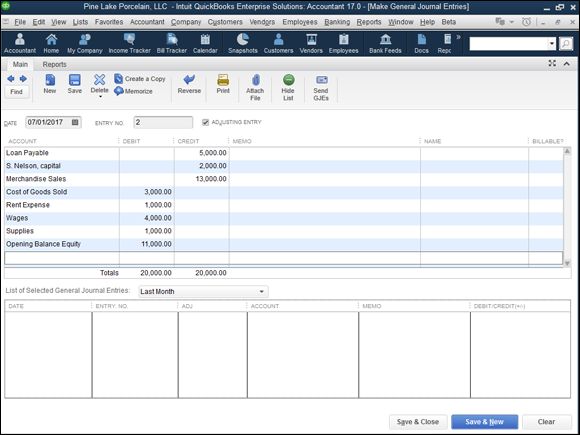

Suppose that you have the trial balances shown in Table 1-2 . Note that in this example (unlike the preceding example), the first account shown — the one with $5,000 — is a bank account.

TABLE 1-2 A Trial Balance

|

Account |

Debit |

Credit |

|

Checking |

$5,000 |

|

|

Accounts receivable |

5,000 |

|

|

Inventory |

2,000 |

|

|

Accounts payable |

$1,000 |

|

|

Loan payable |

5,000 |

|

|

S. Nelson, capital |

2,000 |

|

|

Merchandise sales |

13,000 |

|

|

Cost of goods sold |

3,000 |

|

|

Rent expense |

1,000 |

|

|

Wages |

4,000 |

|

|

Supplies |

1,000 |

|

|

Totals |

$21,000 |

$21,000 |

Here’s the tricky part of recording this trial balance. You don’t need — I repeat, don’t need — to record all this trial balance information through a journal entry. Because the bank account, accounts receivable, accounts payable, and inventory portions have already been recorded if you added customer, vendor, item, and bank account information during the QuickBooks Setup process, you just need to enter the rest of the trial balance.

Because you won’t be recording all the trial balance, however, your journal entry not only won’t match your actual trial balance, but also won’t balance. To make it balance, therefore, you plug the difference into an account that QuickBooks supplies for just this sort of bookkeeping madness: the Opening Balance Equity account. Figure 1-9 shows this journal entry.

FIGURE 1-9: The Make General Journal Entries window, showing the final part of a more complicated trial balance.