Eliminating Waste in Business: Run Lean, Boost Profitability (2014)

Chapter 1. Areas of Waste

Where Does All the Money Go?

I am not a teacher, but an awakener.

—Robert Frost

In order to look at waste, you first need to develop an understanding of where the waste is created. As described in this book’s introduction, we are not referring to big, grandiose sources of waste like that of Mercedes-Benz or the federal government. Instead, we focus on the ways you might be wasting money on a daily basis—like printing unnecessary meeting agendas and reports, attending meetings, or sending mass emails—without even realizing it. These smaller wastes typically occur because you are doing things the way you have always done them. Only once you begin to realize where you’re wasting money in your organization—be it on processes or on personnel—can you begin to stop the waste.

Where Do Businesses Spend Money?

So, just where do businesses actually spend their money? A snapshot of where “the average” business spends its money is a bit irrelevant because all business are so radically different. A manufacturer or retailer, for example, will have a lot more inventory on hand than an accounting firm or hospital. In turn, a hospital or accounting firm may incur more in labor costs than a manufacturer or retailer. By the same token, large corporations spend their money in radically different ways than small businesses.

While it is obvious that a manufacturer will have more inventory than an accounting firm, it makes no sense that large companies tend to be more wasteful than small companies. For the individual consumer and businesses, it seems that the more you have, the more you waste. It is easy to find an example of the small business owner using an old folding table as a desk or even buying thrift shop furniture, but this is rare in large corporations. Likewise, corporations have expenses that small businesses would never incur: political lobbying, dividend payouts, and different tax and benefit expenses and deductions. Nevertheless, in all businesses there are some common themes about where money is spent.

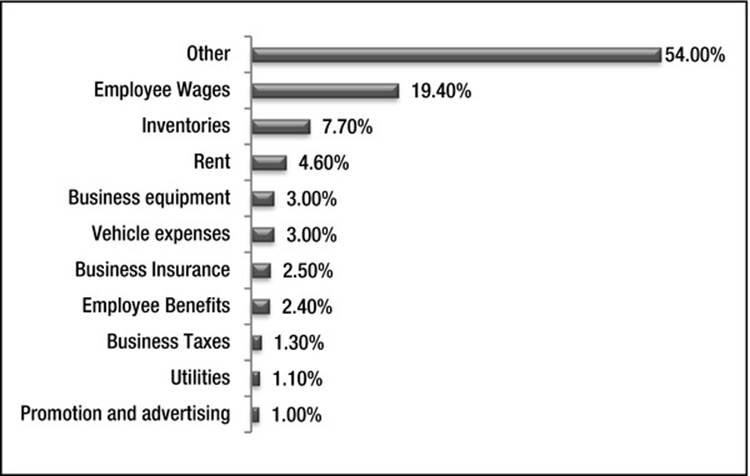

![]() Note As we will discuss later, we are not fans of benchmarking. We do not want you to look at Figure 1-1 as an example that you should follow. It is our position that all businesses are doing some things well and some things very poorly. Averages tend to lump that all together and provide a fuzzy picture.

Note As we will discuss later, we are not fans of benchmarking. We do not want you to look at Figure 1-1 as an example that you should follow. It is our position that all businesses are doing some things well and some things very poorly. Averages tend to lump that all together and provide a fuzzy picture.

Figure 1-1. Average Small Business Expenses1

Figure 1-1 looks at the way the average small business in America spends its money. (These are figures from small businesses. Large businesses have radically different spending patterns.)

As you can see from Figure 1-1, roughly 20 percent of income is typically spent on employees (not including benefits). This doesn’t mean that this is what expenses necessarily should be; it is simply what is being spent now. No one should ever look at another company, even in the same industry, and base their hiring and firing decisions based upon that benchmark. Every person, resource, and company is different. Inventories, while averaging 7.7 percent, could be 0 percent in a pure service business or as high as 20–30 percent for a manufacturer or retailer.

![]() Note No company should ever base major decisions, such as hiring or firing, on what another company, even in the same industry, does.

Note No company should ever base major decisions, such as hiring or firing, on what another company, even in the same industry, does.

WAGES ACROSS THE BOARD

Some extremely labor-heavy service-type businesses will have much higher wage percentages than shown in Figure 1-1. Industries with the highest median percentage of operating expenses devoted to salaries, according to the Society of Human Resource Management, include health care services (52 percent), for-profit services (50 percent), educational services (50 percent), durable goods manufacturing (22 percent), and construction/mining and oil/gas (22 percent). Retail/wholesale trade (18 percent) has the lowest median percentages of salaries as a percentage of operating expense.2

Note in Figure 1-1 that the Other category is enormous (54 percent). This is of course due to the extreme diversity of business and its varying needs. While there is obviously a large amount of waste in this category, the point is that you can reduce expenses in every category. It is not just about paper and cleaning supplies. Instead, this book is about every little microbe of waste. In what ways are you wasting money or time just because you are doing things the way you have always done them? In what ways are you wasting money or time because you don’t understand how to use new technologies and analytical tools? In what ways are you creating waste because you have yet to adopt new technologies and analytical tools?

The Seven Areas of Waste

We have outlined this book based on the functional areas within companies, almost like departments. These “departments,” or areas of waste, include:

· Management and corporate strategy

· Marketing and advertising

· Sales

· Human resources

· Technology

· Finance and accounting

· Business operations

It’s important to understand that the areas discussed here and in the following chapters are by no means departmental issues. In fact, departmentalization, or creating silos, is often a tremendous cause of waste. Whether you are the president of a company or a middle manager of a single department, these seven departments represent waste that is company-wide and should affect every decision you make. For example, if you are in marketing, don’t read the marketing chapter and skip everything else. You might have tremendously efficient marketing strategies and execution tactics, but have tremendous waste by having twice the necessary employees. Likewise, as an HR manager, you can’t accurately determine many employees to cut if you do not understand any of the strategies and objectives of each functional level.

![]() Note Departmentalization itself creates waste.

Note Departmentalization itself creates waste.

Let’s look at each of these areas of waste in more detail.

Management and Corporate Strategy

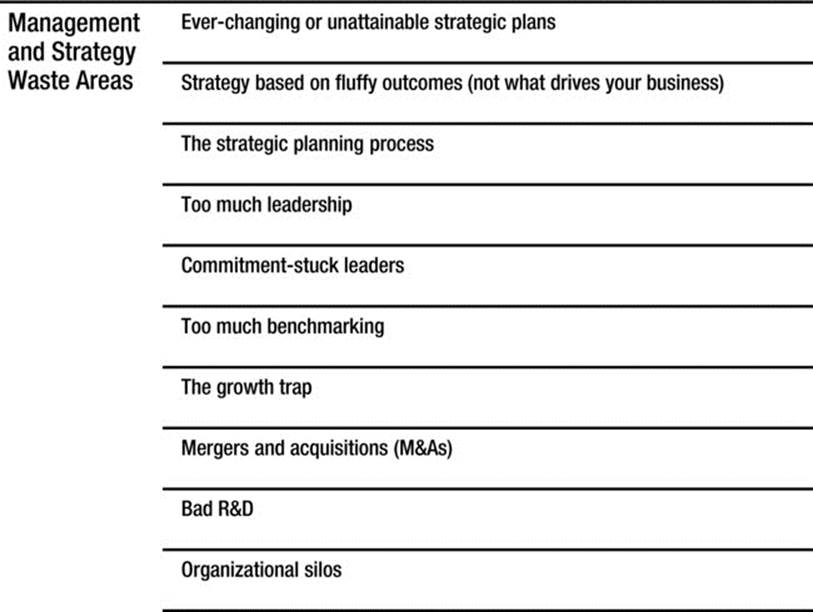

Chapter 2 focuses on waste from management and strategy. The way many strategies are set up today leads companies to be inefficient. Typically, companies develop fluffy, unattainable strategies, such as “to be the best in class.” Then, managers communicate these ideas to the workforce. Employees on the front lines are left staring at each other, with no idea what to do. What does the frontline employee do to be “best in class”? When employees cannot achieve this “goal,” sales go down. Then, management realizes the problem through some lagging indicator, such as sales, and holds a strategic planning session at the country club. The employees feel demotivated by this waste at the Country Club when sales are down, so they work less, causing sales to decline further. Eventually, layoffs are necessary. The employees feel even more upset than they did before. Management is even more upset. This time, they have a strategic planning session in Napa Valley. After all, they seriously need to get away from it all. They spend $34,000 on benchmarks to review during the retreat. Management comes back from this retreat with extremely forceful goals for the employees to follow, based on what the competition is doing. They put up banners throughout the building with sayings about how everyone should “strive for excellence.” Employees feel belittled and burned out. Service decreases. Can you see where this is going? Does it sound familiar?

![]() Note Enormous waste is created by the strategic planning process.

Note Enormous waste is created by the strategic planning process.

So much waste is created by the strategic plan. Waste because the strategic plan is not measurable, and waste from the process of actually creating the strategic plan.

A lot of waste is created because of a misguided desire to grow. Business schools teach us to be concerned with growth. By the way we fund organizations, we are incentivized to grow in order to increase the value of the company. Private equity firms or large investment groups evaluate companies to determine the equity they can build in order to sell the companies for a higher price—when, in fact, there is a point in any business where the business is big enough, and further growth can actually harm it. We all know inherently that greed is destructive, but we seem to forget this when running businesses.

Common growth strategies include mergers and acquisitions (M&As) and price wars, among others, which also result in waste. As we show in Chapter 2, M&As, on average, cost more money than they make. In most M&As, management assumes that 1 + 1 = 3, when in reality 1 + 1 = 0, wasting company resources and time. Leaders need to think twice every time they consider a growth strategy that includes a merger or acquisition and evaluate other options, such as joint ventures or development of new competencies.

Additionally, the work that executive management does around product development and strategy may cause work and expenses that are in excess of the benefits. Because of the desire to grow and the inability to be happy with what the company does well, leaders may decide to create new core competencies. Sometimes, this is a necessary strategy, but at other times, it will only drive mediocrity and cause the organization to lose its identity. In Chapter 2, we discuss when it is time to diversify your skills and when it is time to exploit your current skills to their maximum potential.

![]() Note The perverse desire to grow, especially through strategies like M&As and new product development, creates waste.

Note The perverse desire to grow, especially through strategies like M&As and new product development, creates waste.

Another cause of managerial waste are the boundaries that companies put between departments. In efforts to perform well against budget expectations and get positive performance reviews, department managers tend to focus on the success of their individual department instead of the success of the organization as a whole. Managers may add to administrative expense by charging other departments for services provided in order to account for the activities they perform. Also, in order to show improvements, the managers may make process changes or stop offering services to other areas in the organization, which cause additional expenses in other areas that are greater than the savings incurred by their group. Building measurement systems and business processes that span across the organization and that focus on the overall health of the organization will reduce the waste.

In addition to all these areas, Chapter 2 also discusses strategy metrics—or rather the fact that there actually shouldn’t be any. While every other chapter of this book strongly professes the need for metrics, Chapter 2 warns against them. You should not be looking at overall, strategic-level indicators, such as profit and return on assets, as a guide to the health of your organization. Instead, you should be looking at all the other metrics that measure each individual process that the company is doing. The manager’s job is to incorporate these metrics and make decisions from them. It is not until these activities are mapped out that overall lagging indicators like profitability will make any kind of sense.

The source of strategic waste is described in Chapter 2 and shown in Figure 1-2.

Figure 1-2. Waste from Strategy

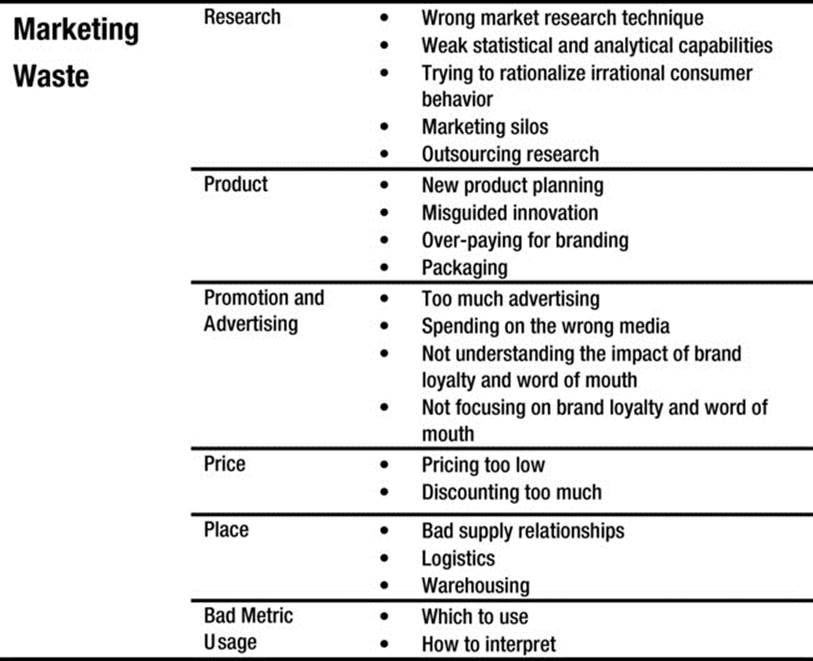

In Chapter 3, we focus on how waste is generated from marketing and advertising. Most companies do some kind of market research, but few do it well. Marketing professionals tend to shoot from the hip when doing market research. Whether it is a basic lack of knowledge of the statistical skills or sheer laziness, this haphazard methodology usually leads to poor decision making and lost opportunities. We talk about the many mistakes that we have seen and how you can conduct effective research that has real meaning.

In a similar vein, faulty research leads to faulty product decisions. Having poor or no product-development processes, along with faulty research, leads to waste within product development. We cover this in Chapter 3, along with the extremely valuable concept of brand loyalty. If managers do not take the time to develop and nurture brand loyalty, they will spend way too much time and money on unnecessary promotional efforts.

On that note, while watching the morning news last week, we saw an advertisement for selling bone marrow. It was running at 5:45 A.M. The question that we had was, “How many people who might give bone marrow are watching TV right now?” Chances are, the biggest portion of this target market is college students, who likely aren’t watching the news in the morning. Then, following the bone marrow commercial, we saw several back-to-back ads for local car dealerships. Again, this shows no understanding of the target market. The huge majority of people make their car-buying decisions today by doing research online.

![]() Note Traditional market research techniques and advertising are hugely wasteful. Marketers should consider big data options for market research, customer satisfaction, and word of mouth before they think about advertising.

Note Traditional market research techniques and advertising are hugely wasteful. Marketers should consider big data options for market research, customer satisfaction, and word of mouth before they think about advertising.

Companies assume that certain marketing and advertising methods are necessary because that is what everyone else is doing, or once again, because they have always done things that way. In our last book, When to Hire or Not Hire a Consultant: Getting Your Money’s Worth from Consulting Relationships,3 we discussed a restaurant owner who wanted to increase his presence on Facebook to get a younger crowd in his restaurant, when all he needed to do was modernize his menu. In this example, as with many business misconceptions, the owner did not understand his target market. Rather than research what the real issue was and fix the root cause, he chose to do what everyone else was doing. We not only talk about the mistakes that people make when considering advertising methods, but also how to calculate the effectiveness of advertising so that you can learn from your mistakes. Of course, there are times when it makes sense to jump on the social media and mobile bandwagons. We also discuss how to measure the effectiveness of these tools.

The issues examined in Chapter 3 are shown in Figure 1-3.

Figure 1-3. Waste from Marketing and Advertising

Sales

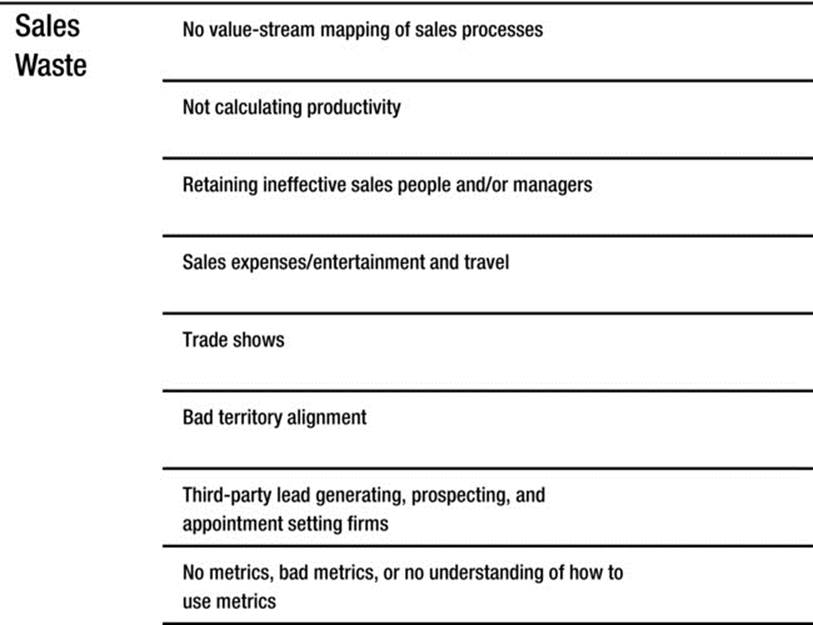

In Chapter 4, we discuss sales productivity and waste in sales cycles. Sales has a long history of being filled with people with “good personalities.” There was seldom any science to sales, let alone much use of analytics. These mindsets need to go. The sales processes should be mapped using value stream mapping just like in manufacturing. Likewise, you must examine productivity and other measures. Sales needs processes, metrics, and analytics as much as any of the departments in the business. Without these, the entire sales department becomes a source of waste.

![]() Note Everyone in sales should use value-stream mapping. Likewise, productivity metrics should be used.

Note Everyone in sales should use value-stream mapping. Likewise, productivity metrics should be used.

We also talk about other antiquated sales activities, such as golfing with clients or high-entertainment expenses, and how these are wasteful. Even though there is a natural reciprocity phenomenon when these activities occur, studies show that high-entertainment spending and spending more time with the client actually produces lower sales. We discuss what sales professionals should actually be doing to maximize their value and drive sales. This includes spending more time planning for sales and serving current customers and less time “just stopping by to check in.” As company budgets get tighter, it is necessary to focus our travel expenses on trips that provide real value. There is no success in being on the road all of the time. Instead, resources should be aimed at the company, and they should provide real value. Sales are made by strategizing and being analytical about accounts, not by how much time you spend with the clients.

![]() Note The less time you spend with clients, the higher your sales will be!!! Strategy is what’s important, not golf.

Note The less time you spend with clients, the higher your sales will be!!! Strategy is what’s important, not golf.

The topics covered in Chapter 4 are summarized in Figure 1-4.

Figure 1-4. Waste from Sales

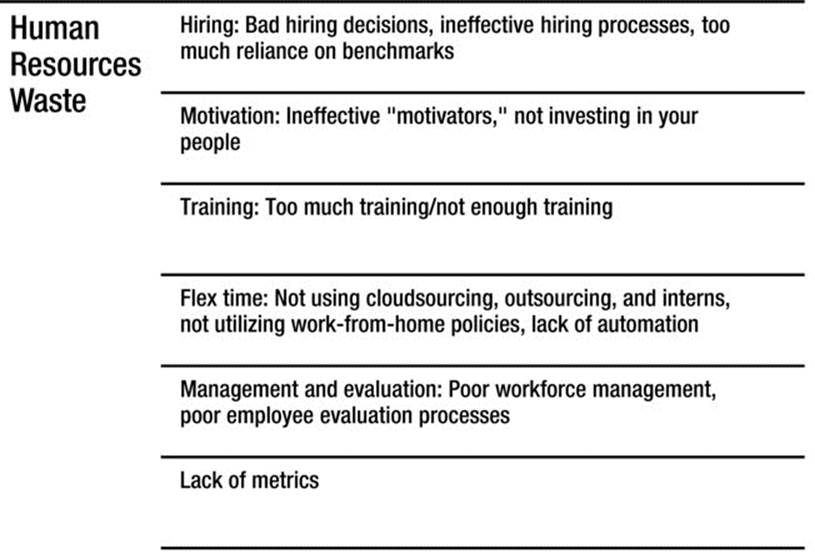

Human Resources

Human resources (HR) is, in theory, a department whose primary function is to provide services to the entire organization. Even though as a support function it should help everyone, the processes implemented by human resource professionals are typically enormous sources of waste.

Recently we heard from a friend about someone applying for a finance position in a local company that employed a few hundred people. This person’s resume never made it to the hiring manager because she was flagged by human resources. The obvious initial reaction is that she must have some kind of issue that would keep her from functioning in this job. This applicant was a vice president at a national bank with an exceptional record. She was perfectly qualified. Her resume was removed from the pool of applicants because she had no experience in the company’s specific industry. This qualification had been determined by someone in HR. This is a reasonable requirement for engineering or some direct contributor role, but it seems like a bizarre one for a finance director.

We chose this example because it gets to the root of the problem. At some point in the last few decades, human resources forgot that its job is to advise and help management. Now it operates like its job is to control management. Whether or not this is true in your firm, the lesson is still the same. Any time a manager makes decisions without proper understanding, analysis, and relevant data on which to base them, you have inherent waste. Employees in a different department than yours rarely have the proper data to make good decisions for your department, at least not without your input.

![]() Note Every decision made in every company should be made with accurate and relevant data analysis.

Note Every decision made in every company should be made with accurate and relevant data analysis.

Beyond poor decision making and lack of understanding, the human resources role creates waste within the hiring process. Much of this waste is because, like so many other things, they do things the way they have always done them.

Consider this example. In academia, hiring takes place once a year. We send two-three professors to a once-a-year conference. This costs a few thousand dollars for rooms, food, travel, and conference registrations. During this conference, about 50-75 interviews take place. So, comparing the expenses to the number of interviews, this might be an efficient use of resources. However, after meeting face-to-face with all of these candidates, the top three or four are invited back to campus for “campus visits.” During these visits, each candidate spends two or three days in town. The university pays for their airfare, local travel, hotels, and food. And it’s not just food for the candidate. Every meal is planned with the candidate and several other faculty members. All totaled, these visits cost a few thousand dollars each. Also, there is paperwork, faculty members’ time, and committee meetings. Each search ends up costing the university tens of thousands of dollars.

We mention this scenario because this is an obvious case where the existing processes create thousands of dollars of waste for each position that is filled. You could argue that hiring the wrong employee creates even more waste, so the process needs to be done right. However, this expensive process doesn’t guarantee better hiring decisions. It happens, once again, because this is the way things have always been done. With all of these expenses—all the steak dinners for four and breakfasts that no one wants—we can still make major hiring mistakes. These particular expenses do not enhance the hiring process. There are no metrics in place to determine the added value of any part of the process and really no post-hire reassessments. Likewise, new technologies are not even considered. There are opportunities to improve practices like these. For example, many companies use tools like Skype to reduce interviewing costs.

![]() Note Every expense should have an associated ROI analysis.

Note Every expense should have an associated ROI analysis.

Once they hire new employees, companies seem to have remarkably little idea how to motivate them to increase performance. The ubiquitous pizza party or fancy banquet for a job well done is a common business practice, although there is no proof that they actually increase performance. In fact, most people dread the obligatory need to attend such events. Another common motivator is the idea of casual or blue jean Friday as a motivation. Do these things actually motivate employees to perform better? By the same token, team and organizational-based bonuses that don’t tie to individual performance, don’t incentivize performance. Once again, where was the measurement and analysis? When were employees asked what they wanted? We discuss real motivators in Chapter 5.

The best companies are ones that invest in their employees. We have worked for organizations where many people chose to work there for lower than market wages because of the attractive benefits package. These employees tended to be more conscientious and loyal because their focus was less on the weekly paycheck and more on the overall relationship with the company. Some students graduating from undergraduate degree programs will not consider working for companies without reimbursement programs for earning a master’s degree. Yet, benefits such as healthcare, retirement, tuition reimbursement, and paid time off are frequently looked upon as areas where money can be saved with little or no productivity loss. This is a faulty assumption.

Making the decision not to support employees who care about their health, future, or work-life balance is making the decision to lose those employees. Aren’t these the employees you want? We have heard business leaders claim that they pay for employee education, only to have those employees leave the business. This is a risk worth taking. Not only do you have a motivated employee while she is working on improving her education, you also have the benefit of the education while she is working on her degree. We will talk about these and other decisions that human resource leaders make. They might look good on paper, but they cost the company money.

![]() Note Managers must truly understand what motivates their employees.

Note Managers must truly understand what motivates their employees.

Additionally, with technological advancements, employees have more flexible work schedules and outcome-based work processes. We also have workforce models where we can use part time or contingent workers to minimize costs. We know workers are 12 percent more productive when working from home.4 Employees who work from home report higher job satisfaction and have 50 percent lower attrition.5 So, it is a shock to see more and more office buildings popping up all over the place. There are also more ways to automate processes and measure efficiencies. We talk about why some of these improvements are good, whereas others are hurting the companies that use them.

The sources of human resource waste are shown in Figure 1-5.

Figure 1-5. Waste from Human Resources

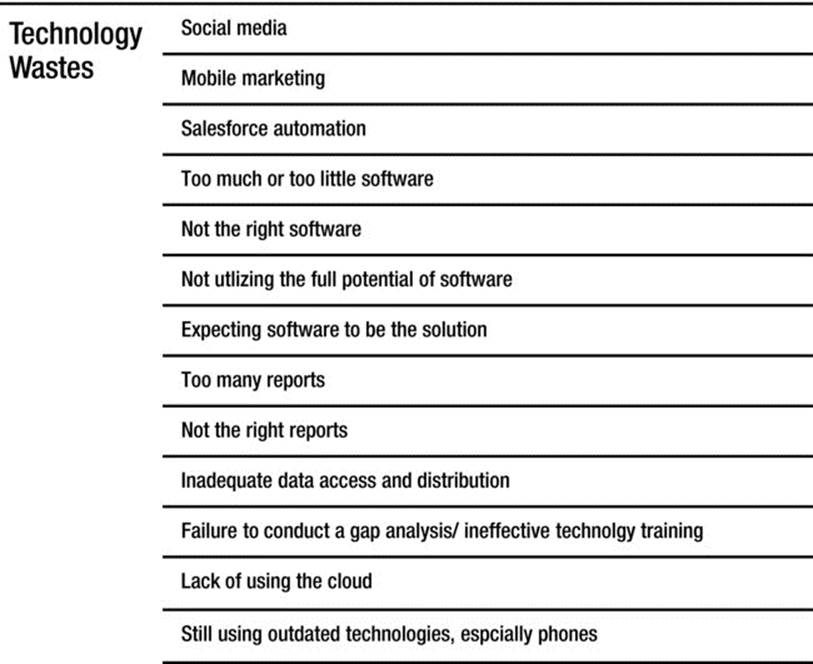

Technology

Technology can be a good way to increase efficiency and effectiveness when it’s used properly. It can also be a tremendous source of waste. We have seen companies without good information technology systems and companies with hundreds of software packages that are not integrated. We have also seen companies that still do most things by hand, using simple Word documents and Excel spreadsheets, instead of learning how to automate processes. There is no magic formula for the correct way to manage your technology, but there are some good tips to follow that will reduce the risk of misusing it.

Software can serve multiple purposes and be a key piece of any company’s success. Whether it is an Enterprise Resource Planning (ERP) system or Microsoft Office, the software expense should have a return on investment. Companies often have a base software suite, such as Microsoft Office (Word, Excel, PowerPoint, and Outlook), Lotus Symphony, or Google Docs to perform routine tasks such as word processing and basic computing. In addition to this base software, there are other software needs that are unique to each business. Each piece of software should have a specific purpose.

Companies should also understand how to use social media effectively, and not just be trying to follow the latest fad. Technology advancements are not limited to Facebook and Twitter. We discuss many aspects of social media usage. Also, companies should understand how to use social media and other technologies to help the sales force’s efforts. In Chapter 6, we discuss how to utilize big data to identify opportunities. We also show how sales force automation and customer relationship management software can increase the capacity of each sales person.

![]() Note Every software and hardware expense must have an ROI.

Note Every software and hardware expense must have an ROI.

Another technology is the use of reports. I (Dave) once worked with an IT manager who questioned the necessity of all of the reports that his team created and managed. He decided to move all of the reports to a different area on the company’s network to see what would happen. After about two weeks, he had received four phone calls about missing reports, which he addressed by replacing the reports for those users. In the following two months, he heard from seven other employees who were looking for their reports. In the end, his experiment showed that less than 10 percent of the reports that his department created were actually used. Reports can be a huge source of waste. The strategies of some organizations are to push reports to employees in order to ensure that nothing is missed. When this strategy is used, the reports are deleted before many of those users read them. Another strategy is to teach users how to run reports as needed. In this case, if the method to run reports is simple, the method may be effective, although the learning curve may keep many users from ever running reports. We discuss how to create, use, analyze, and kill reports.

Data access is an ongoing issue in most organizations. Most people agree that salary and personal information should be kept secure. In the banking industry, specific customer information must be kept secure. The government has regulated the use of healthcare information to keep private information secure. But what is the right data access policy? We have found that companies either use too loose of a strategy, relying on worker ignorance of the IT systems to secure data, or too stringent of a strategy, keeping workers from accessing the information they need to do their jobs effectively. We discuss the benefits and issues with both strategies, so you can formulate a strategy that will keep your data secure without causing waste or inadvertently making the data less secure in the process.

A couple of common jokes in the information technology field are the concepts of P.I.C.N.I.C. (problem in chair, not in computer) or I.D.10T (idiot) errors. This is not the fault of the individual workers but rather those techno-savvy workers who set up software and policies without training users on how to use the software. I will never forget hearing in my early career about a vice president who was told by the IT manager to “go to My Computer” while on a phone call. This vice president left his office and walked to the IT manager’s office. The IT manager meant to have the vice president click on the “My Computer” desktop icon in order to help troubleshoot the problem, but his lack of basic computer knowledge made this a long-standing joke about how poorly some people understand technology. Implementation of any software must include effective training for its users.

Any office-based role must have a minimum computer knowledge requirement for employment. We cannot leverage the potential efficiencies from technology without this knowledge. There are tenured college professors teaching students today who still use overhead projectors with materials that were created in the 1980s or earlier. There are business executives who have their administrative assistant print all of their e-mails because the executive cannot use the computer. We know people in VP roles who do not know how to use PowerPoint, so they must have an assistant create presentations for them. Most businesses use technology, so your expectation of your employees and leaders must include knowledge of that technology. We talk in Chapter 6 about how to create gap analyses and formulate capability build training for the use of software. These two tools can help overcome some of the large source of waste involved with technology implementations.

When implementing technology, IT leaders often tend to take one of two approaches: customize nothing or customize everything. There is normally no focus on understanding the best process and either selecting the software based upon the process needs or customizing the software to fit the best process. When businesses choose to implement new technology, the IT team usually selects the technology before they truly understand the business’s needs. We talk about the right process to ensure that technology purchases actually improve your work.

When companies choose to implement new technology, it is likely because they are replacing outdated technology and hoping for improvements in operations. Unfortunately, business leaders often choose new technology that mimics the technology they are replacing. We discuss how to access current technology and how to decide if new technology is necessary. We also focus on how to maximize the effective use of any new technology. This discussion explores the use of cloud technology, including SaaS (Software as a Service). As we show, organizations can save over 90 percent of IT operating costs by utilizing the “cloud.”

The topics discussed in Chapter 6 are shown in Figure 1-6.

Figure 1-6. Waste from Technology

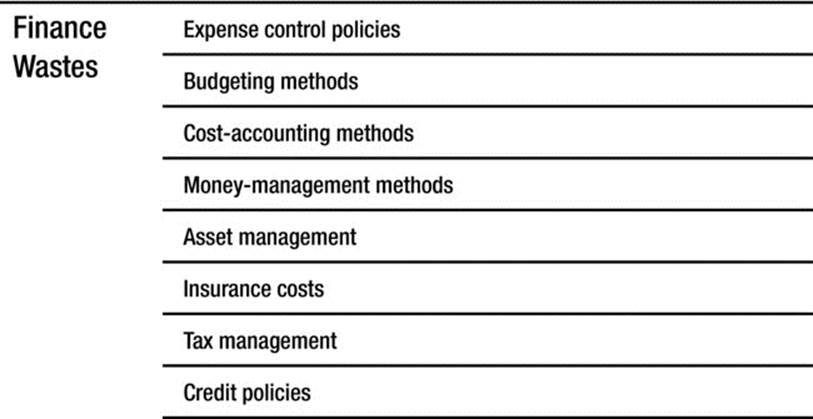

Finance and Accounting

The processes of finance and accounting include managing investments, obtaining capital, accurate reporting in accordance with regulatory requirements, and controlling expenses. Unfortunately, these processes can cause waste. When business owners think they are controlling waste by managing it better, they are, in reality, creating waste.

With the goal of controlling expenses, we have seen ridiculous approval processes put in place by leaders. A division president of a very large manufacturing organization with over 150 employees enacted a policy whereby every expense over $25 needed his approval. This added waste and demotivated employees by instilling a sense of mistrust. Other organizations we have seen required that routine purchases for supplies needed up to four signatures to be approved and an employee reimbursement needed three signatures, regardless of the size of the expense. The adage, “when multiple people are responsible for something, no one is” holds true here. We talk about how to improve these expense-control methods in an effort to reduce administrative expense and improve accountability.

Travel policies may also drive up expenses. We once worked with a person who remodeled his basement with the money he accrued by renting a car for all long road trips and then charging the company mileage for the distance traveled. The expense versus reimbursement for him ended up being quite profitable. Likewise, as we explain in other chapters, travel on the whole is quite unnecessary today, so sometimes the whole category can be wasteful. We look at how to not only improve the process for capturing travel expenses, but also how to reduce actual travel expenses.

Additionally, the budgeting processes used in many companies are ineffective and costly. The basis for the new budget cycle is often the prior year’s performance, with some modification based upon the new sales projections. This process encourages managers to spend their budget so that they can get an equivalent budget the following year. We have witnessed this many times and heard from other managers who will admit to this process. It can be further proven by looking at the expenses throughout the course of the year. We talk in Chapter 7 about how to implement a zero-based budget strategy to eliminate this wasteful spend-and-budget process.

![]() Note Implement a zero-based budget strategy to reduce waste caused by faulty budgeting practices.

Note Implement a zero-based budget strategy to reduce waste caused by faulty budgeting practices.

Budgeting is not limited to the annual budget. New projects, products, and services often include a pro forma with a list of projected revenues and expenses. We have frequently noticed a trend across multiple companies where the projections on the revenues don’t come to fruition while the expenses are equal to or greater than projections. We discuss how to identify and avoid being trapped by fake projections or other fake numbers through accurate forecasting.

Traditional cost-accounting methods make it difficult to manage expenses and drive real improvement in an organization. We discuss how to implement activity-based costing for a better view of the cost drivers in the organization and to see movement from improvement efforts.

As part of the purchasing discussion, we explore capital expenses. One key decision around capital expenses is the lease versus buy question. Once reserved for equipment and building purchases, this decision has been expanded to other purchases, such as software. As with any decision, there are reasons to adopt either method. We explore those reasons and identify the potential wastes they cause.

If you’ve spent any time watching the Hoarders: Buried Alive show on A&E, you are familiar with some of the personal issues that people face when they cannot let go of possessions due to personal attachments. This happens within organizations as well. Brad Pitt said in Fight Club that “The things you own, own you.” This applies to businesses. We discuss how holding onto unneeded assets can be detrimental to an organization. These often-unlooked issues can be a large source of waste for companies. We highlight some of these in Figure 1-7.

Figure 1-7. Waste from Finance

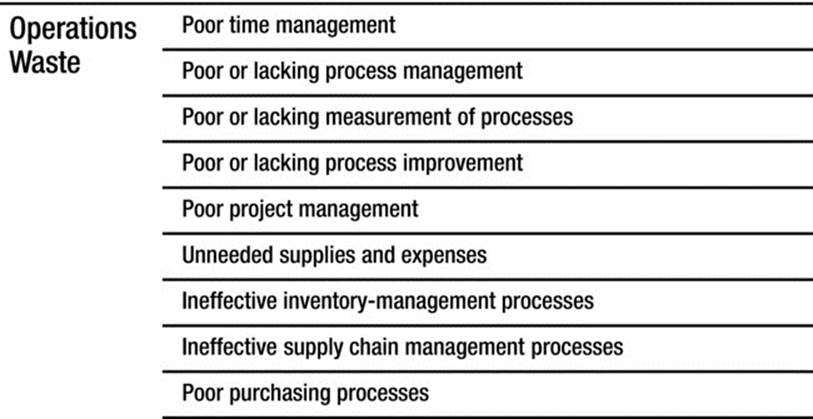

Business Operations

It may sound too obvious to say, but every business needs to operate. However, when many people hear “operations management” or “process improvement,” they might think those terms apply only to very large businesses or to manufacturers. That is absolutely wrong. Every business has operational needs.

In the early stages of a business, only critical functions are created and supported. Large-scale operational efficiencies are never really considered, thought about, or maybe not even needed at this phase of the business. When survival is the name of the game, normally people are quite frugal. As the business grows, more processes are created to support this growth. At some point, these processes become redundant and less effective. This happens due to lack of a grand design of what the business should look like at various phases. We discuss how to address these wastes through business process analysis. In these analyses, we look at the work environment and use Lean Six Sigma techniques to identify root causes of waste. This kind of waste is often due to redundant or inefficient processes, resources, facilities, equipment, and inventory. Many of these processes deal with the mundane, everyday processes that every employee gets trapped doing.

For instance, most professional workers attend almost 62 meetings a month.6 If you account for travel time of 15 minutes between each meeting, this is over 50 percent of the working time. Over 50 percent of the meeting time is wasted,7 which means that more than 25 percent of a professional worker’s time is wasted in meetings. The average small business owner’s time is worth over $250.8 If you assume a 50-hour work week, the average business owner wastes over $162,000 a year in meetings! In Chapter 8, we demonstrate how much money is wasted in meetings based on different types of employees and their average salaries.

![]() Note The average small business owner wastes $162,000 a year in meetings.

Note The average small business owner wastes $162,000 a year in meetings.

As we have said it many times, we have these meetings because it is what we have always done. We buy into business “myths.” One of these myths, brainstorming, is as rampant as an urban legend. The concept was originally created by an advertising executive trying to sell books. It has never been proven to be effective and, in fact, has been shown to be detrimental to group success, in terms of quality and the number of ideas generated.

For this reason, managing time and prioritizing task work are important skills to have in a business. We talk about meeting-management techniques that can help maximize the productivity of meetings, as well as limit the number of them. We also discuss how to manage your time and prioritize tasks to ensure that the time when you are not in meetings is well spent.

Additionally, one fundamental issue in business operations is the concept of process management. Process management combines relevant metrics that show operational performance, all in a time frame that allows managers to react to variations in performance.

Lord Kelvin, a British physicist from the late 19th Century, has two famous quotations that deal with measurement. The first is, “to measure is to know.” This deals with the fact that most people have opinions, but only those with data to support their opinions can be sure of the validity of their opinions. The second quote is, “if you cannot measure it, you cannot improve it.” This is a fundamental characteristic of Six Sigma process improvement; in order to show improvement, you must have a measureable baseline and a post-improvement measurement, and then be able to show a statistical difference between the two. Lord Kelvin is correct on both accounts, which is why the process-management portion of this book is important.

Although this section of the business operations chapter focuses on process management, we talk about process management throughout all of the chapters. When we talk about process management, we explore how to identify what measurements help you see process changes before they affect the outcome. In each chapter, we review which key performance indicators show how successful you are in each area of your business.

As we explain throughout Chapter 2, we all learned in high school algebra that Y=f(X). This states that the output (Y) is a function of the inputs (Xs). This simple formula holds true for business processes as well, and we look at how to identify which inputs drive the outputs you desire. These will become the key process metrics that you will monitor on an hourly, daily, or weekly basis to help drive monthly or quarterly performance. By using a combination of these process metrics and visual cues of performance gaps, you will be able to identify where process improvement or redesign is necessary.

With the effective process management that we discuss throughout the book, you will identify performance gaps that you will need to improve. In the process-improvement portion of this chapter, we explain various process-improvement techniques and how to apply them to business situations. These process-improvement techniques include Six Sigma (improve quality and process effectiveness), lean management (improve process efficiency), and the theory of constraints (remove process bottlenecks).

Additionally, we discuss how simple items such as paper, Post-It notes, filing cabinets, and printers drive cost inefficiencies. Along with identifying these wastes, we show you how a change in business processes and effectively leveraging technology can eliminate these wastes and provide a real return on investment. Inventory is one of the eight wastes identified in lean manufacturing. This is because this money is tied up and can’t be used to meet the customers’ needs. Inventory also hides problems. Therefore, effective management of inventory is a key step in managing a company. If you carry too much inventory, problems that you need to solve may hide from you.

Along with justifying which supplies are used in the business, we discuss warehousing and distribution methods. This includes how to choose the right methods for different types of businesses. We explore common mistakes in distribution and inventory-control decisions so that you can avoid them.

Every company needs to purchase products and services, yet so many companies create waste through its purchasing practices. The old way of purchasing was to focus only on price when making a purchasing decision. After the product or service specifications were created, the purchasing professionals would look for a supplier to provide that service. As long as the supplier was able to provide what was needed, the cheapest option was pursued. As part of this decision-making process, transportation fees or taxes are added to the base cost of the item. Unfortunately, this basic practice is still in use and drives waste. We discuss more effective practices, which consider the total cost of purchasing with the aim of driving down not only purchasing costs but also operational expenses. The summary of the topics discussed in Chapter 8 is provided in Figure 1-8.

Figure 1-8. Waste from Operations

Appendix

In the final section of this book, you’ll find the appendix. When we initially came up with the idea to write a book about business waste that is different from the thousands of waste books on the market, we had a few areas of business in mind (ones where we consistently see egregious waste). As we worked on this project, researched information on waste, and brainstormed waste we had seen or experienced, we realized that this book could be more of an encyclopedia of business waste rather than a simple book outlining some specific wastes. For this reason, the appendix of this book serves as a key resource for our readers.

Because process management is a key and often poorly executed area of business, we have decided to incorporate elements of process management throughout this book. Although process-improvement techniques are used throughout this book, we intend this book to be a reference guide. We outline various process-improvement techniques and templates in the appendix for you to use.

Conclusion

We designed this book to be different from other waste books available on the market. The book is organized into traditional functional areas, but we show how waste in some areas causes waste in other areas. By examining the common business functions and their fundamental process wastes, we show why you should question all of the processes. We hope that you adopt the mindset, “if you can’t measure it, don’t do it.” Every resource, process, and activity should produce a positive ROI. We hope that this is an eye-opener to the enormous amount of waste that exists in all organizations. There are formulas, tools, and questions to help you work through the waste in your organization and realize the overall benefits that you can achieve.

1 Jason Del Rey, “Infographic: How Small Businesses Spend Their Money,” http://www.openforum.com/articles/infographic-how-small-businesses-spend-their-money/, July 19, 2011.

2 Society of Human Resource Management, “Salaries as a Percentage of Operating Expense” http://www.shrm.org/Research/Articles/Articles/Pages/MetricoftheMonthSalariesasPercentageofOperatingExpense.aspx, November 1, 2008.

3 Linda M. Orr and Dave J. Orr, When to Hire or Not Hire a Consultant: Getting Your Money’s Worth from Consulting Relationships (New York, NY: Apress, 2013). p. 82–83.

4 Steve Cooper, “Boost Productivity by Working from Home, Really!” http://www.forbes.com/sites/stevecooper/2012/08/31/boost-productivity-by-working-from-home-really/, August 31, 2012.

5 Ibid.

6 A Network MCI Conferencing White Paper, “Meetings in America: A Study of Trends, Costs, and Attitudes Toward Business Travel, Teleconferencing, and Their Impact on Productivity,” INFOCOMM, Greenwich, CT: 1998.

7 Robert B. Nelson and Peter Economy, Better Business Meetings (Burr Ridge, IL: Irwin, Inc. 1995). p. 5.

8 David Mielach, “What’s a Small Business Owner’s Most Valuable Assest?” http://www.businessnewsdaily.com/2942-business-owner-time.html, August 2, 2012.

All materials on the site are licensed Creative Commons Attribution-Sharealike 3.0 Unported CC BY-SA 3.0 & GNU Free Documentation License (GFDL)

If you are the copyright holder of any material contained on our site and intend to remove it, please contact our site administrator for approval.

© 2016-2026 All site design rights belong to S.Y.A.